CIO View: April 2026

Image

he easing of geopolitical tensions has reduced immediate tail risks and supported market sentiment, but the global outlook remains fragile amid slower growth, supply driven inflation, and elevated policy uncertainty. Major central banks are expected to maintain a cautious, higher for longer stance, while growth across key economies shows increasing divergence. In this environment, investors should prioritize resilience and diversification, focusing on selective opportunities rather than broad risk taking. Our portfolio positioning reflects this approach across equities, credit, and multi asset strategies.

Busy readers may refer directly to the final section for a summary of our recommended funds.Global Macro: Tail Risks Ease, But Fragility Persists

The geopolitical landscape has shifted following the ceasefire between the United States and Iran, bringing a pause to heightened military activity that had disrupted global trade routes and energy production. This development has reduced near term tail risks to energy supply—particularly around the Strait of Hormuz—helping stabilize oil prices after a period of acute volatility. Nevertheless, prices continue to embed a geopolitical risk premium given the temporary nature of the ceasefire and lingering regional uncertainty.

The moderation in energy driven volatility has slightly eased inflation concerns and improved risk sentiment, supporting equities and other rate sensitive assets. At the same time, traditional safe havens such as gold and the U.S. dollar have softened only modestly, underscoring that investor caution remains intact. Overall, the global environment appears to be transitioning from acute shock toward a phase of fragile stabilization rather than a decisive return to pre conflict conditions.

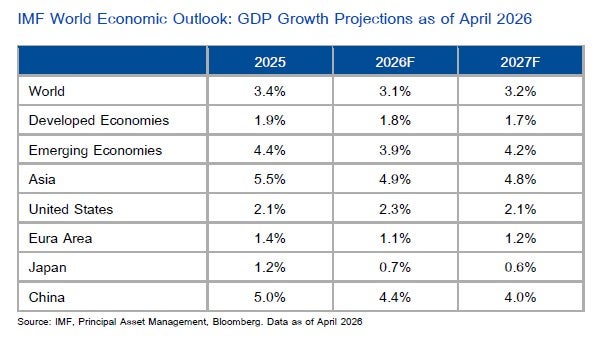

The IMF’s April 2026 World Economic Outlook reflects this more delicate balance. Global growth is projected at 3.1% in 2026 and 3.2% in 2027—below pre pandemic averages—reflecting the combined impact of higher energy prices, tighter financial conditions, and elevated geopolitical uncertainty. Global inflation is expected to rise modestly in 2026 before resuming its downward trajectory in 2027, as supply side pressures temporarily interrupt the disinflation process, particularly in emerging economies.

Among major economies, the IMF expects the U.S. economy to remain relatively resilient, supported by a still healthy labor market despite tightening financial conditions. The euro area remains the weakest among advanced economies, constrained by energy costs and subdued domestic demand, while Japan’s outlook is similarly muted amid structural headwinds.

Image

China delivered a solid start to 2026, with real GDP expanding by 5.0% year on year in the first quarter, up from 4.5% in the previous quarter and comfortably above market expectations. Growth is tracking near the upper bound of the government’s 4.5%–5.0% annual target range. The acceleration was export and manufacturing led, supported by a rebound in industrial activity—particularly in high tech sectors—while services continued to contribute steadily. By contrast, domestic demand remained subdued, reflected in modest retail sales growth, weak private investment, and a continued drag from the property sector. Although the strong headline performance has eased immediate pressure for broad based policy stimulus, policymakers and investors remain cautious about downside risks later in the year, particularly from higher energy costs, external demand uncertainty, and ongoing geopolitical tensions. As a result, growth momentum is likely to moderate beyond the first quarter.

Consistent with this backdrop, the People’s Bank of China kept monetary settings unchanged, maintaining the one year Loan Prime Rate at 3.0% and the five year LPR at 3.5% for the eleventh consecutive month. The decision reflects a deliberate wait and see approach, supported by resilient first quarter growth and a nascent rebound in inflation pressures. At the same time, policy rhetoric remains moderately accommodative, with flexibility to deploy targeted measures should growth weaken later in the year, even as broad based easing remains unlikely in the near term.

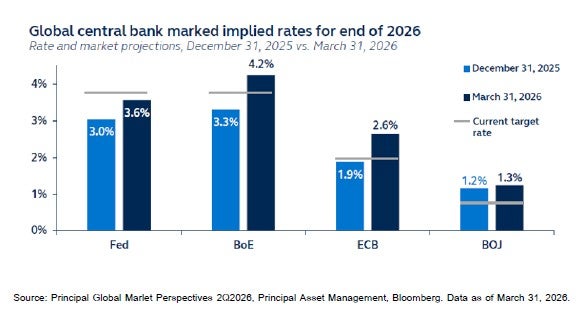

Against this backdrop, market participants broadly expect no policy changes from major central banks at their April meetings. According to the house view of the Principal Global Insights Team, global monetary policy is shifting toward a more hawkish and asymmetric path, with easing delayed and policy divergence becoming more pronounced.

In the United States, the Federal Reserve is expected to keep policy rates unchanged at 3.50%–3.75%. While labor market conditions have softened incrementally, elevated inflation risks—stemming from energy prices and tariffs—argue for caution. Consistent with the Principal Global Insights Team’s view that policy is “delayed, not derailed,” the first rate cut is expected no earlier than September or December 2026, with further easing pushed into 2027.

In Europe, the ECB faces a more constrained policy trade off due to its price stability mandate and greater exposure to energy shocks. The Principal Global Insights Team expects the ECB to retain a tightening bias, with the possibility of one or two rate hikes in 2026 rather than near term cuts. The Bank of Japan, meanwhile, is expected to maintain a gradual normalization bias—keeping policy steady in the near term while remaining responsive to wage and inflation dynamics.

Image

Thailand Macro: Sovereign Stability Amid Limited Policy Space

Moody’s upgrade of Thailand’s sovereign outlook to stable from negative reflects a more balanced assessment of external and domestic risks. Reduced pressure from U.S. trade measures, following lower tariffs on Thai exports, has improved the external backdrop, while strengthening private investment momentum and greater policy continuity have enhanced medium term growth visibility. At the same time, Thailand is preparing emergency borrowing authorization of up to 500 billion baht to mitigate the impact of higher energy prices, support household purchasing power, and sustain near term economic activity. With public debt at around 66% of GDP, policymakers are considering a potential increase in the voluntary debt ceiling from 70% to 75% should additional flexibility be required. Authorities have emphasized that any such adjustment would be temporary, disciplined, and focused on growth supportive measures, consistent with maintaining Thailand’s investment grade sovereign profile.Recent monetary policy decisions reinforce this constrained policy backdrop. The Bank of Thailand’s Monetary Policy Committee voted unanimously on 29 April 2026 to hold the policy rate at 1.00%, assessing the current stance as appropriate amid a weakening growth outlook and elevated uncertainty. The Committee projects GDP growth to moderate to around 1.5% in 2026 and 2.0% in 2027, reflecting the impact of higher energy costs—driven by the Middle East conflict—on production and household purchasing power, alongside softer tourism dynamics. Headline inflation is expected to rise to approximately 2.9% in 2026—temporarily breaching the upper bound of the target range—before easing to around 1.5% in 2027 as supply side pressures subside. Importantly, the MPC emphasized that inflation remains largely supply driven, with limited demand pull dynamics amid subdued credit growth.

Against this backdrop, the Bank of Thailand has reaffirmed a data dependent, wait and see approach, balancing the need to support growth with the need to monitor inflation expectations and financial stability risks. From a policy perspective, we expect the Bank of Thailand to remain on hold at 1.00% for the remainder of 2026. As long as growth evolves broadly in line with the MPC’s projections—at around 1.5% in 2026 and 2.0% in 2027—we do not anticipate a rate cut this year. At the same time, with inflation pressures assessed to be largely supply driven and limited evidence of demand pull dynamics, the likelihood of policy tightening also remains low. This reinforces our view that monetary policy is likely to stay stable, with the Bank of Thailand maintaining a cautious, data dependent stance amid elevated uncertainty.

Recommended Funds: Implementing the House View

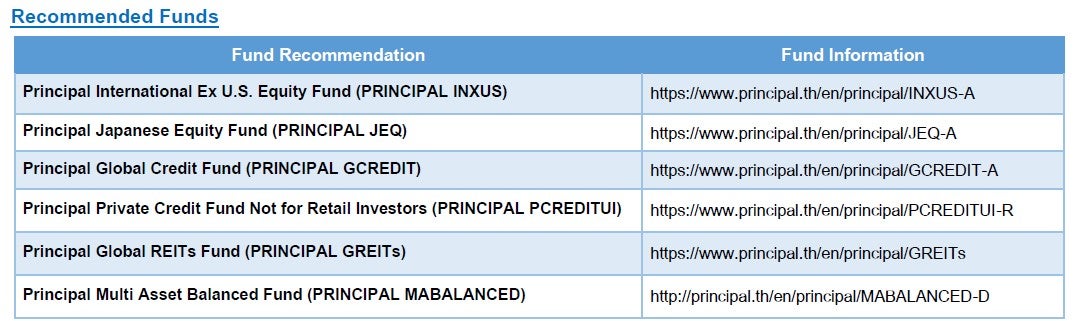

Reflecting the Principal Global Insights Team’s emphasis on resilience, diversification, and selective risk taking, the following funds provide practical portfolio implementation across asset classes:

• Principal International Ex U.S. Equity Fund (PRINCIPAL INXUS)

Diversifies equity exposure beyond the U.S., benefiting from more attractive valuations and improving relative earnings momentum in developed markets.

• Principal Japanese Equity Fund (PRINCIPAL JEQ)

Offers targeted exposure to Japan’s structural reform progress, improving corporate governance, and differentiated growth drivers.

• Principal Global Credit Fund (PRINCIPAL GCREDIT)

Provides diversified global credit exposure, aligned with the house view that resilient corporate fundamentals support income in a higher for longer rate environment.

• Principal Private Credit Fund Not for Retail Investors (PRINCIPAL PCREDITUI)

For eligible investors, offers enhanced income through private credit, where risks remain largely idiosyncratic and supported by disciplined underwriting.

• Principal Global REITs Fund (PRINCIPAL GREITs)

Adds global listed real asset exposure, benefiting from income stability and diversification as growth moderates and rate paths diverge.

• Principal Multi Asset Balanced Fund (PRINCIPAL MABALANCED)

Provides a diversified, single solution portfolio balancing growth and defensive assets, consistent with the house conviction that disciplined diversification remains critical amid volatility.

Image

Disclaimer: Investors should understand product characteristics (mutual funds), conditions of return and risk before making an investment decision./Investing in Investment Units is not a deposit and there is a risk of investment, Investors may receive more or less return investment than the initial investment. Therefore, investors should invest in this fund when seeing that investing in this fund suitable for investment objectives of investors and investors accept the risk that may arise from the investment. PRINCIPAL JEQ has highly concentrated investment in Japan. Therefore, investors should consider the overall diversification of their investment portfolio. PRINCIPAL GCREDIT has highly concentrated investment in United States and Europe. Therefore, investors should consider the overall diversification of their investment portfolio. PRINCIPAL GREITs has highly concentrated investment in United State. Therefore, investors should consider the overall diversification of their investment portfolio. PRINCIPAL GREITs, this fund is concentrated in the property sector. Therefore, if there are negative factors that affect the investment, Investors may lose a lot of money. PRINCIPAL PCREDITUI, mutual fund for institutional and ultra-high-net-worth investor only. PRINCIPAL PCREDITUI, High Risk or Complex Mutual Fund. PRICNIPAL INXUS, PRINCIPAL JEQ, PRINCIPAL MABALANCED, PRINCIPAL PCREDITUI, PRINCIPAL GCREDIT, PRINCIPAL GREITs, have a policy to invest in foreign investments. Investors may lose or receive foreign exchange gains or receive a lower return than the initial investment. The fund and/or the master fund may invest in derivatives for hedging purpose, at the discretion of the fund manager. The funds have a dynamic hedging policy, with a hedging ratio ranging from 0% to 105% of foreign exchange exposure. Past performance does not guarantee future results.