How much money should employees contribute to provident fund?

Working at the company where employer provides certain benefits to their employees more than just the law requires such as "Provident Fund", is a very good opportunity for employees to increase chances to retire as intended. “Provident Fund” is considered as a suitable financial tool for retirement. At present, there are only 20,000 companies that provide provident fund to employees although it is not compulsory for an employer to contribute to a fund. Thus, if your company has provident fund provided as job welfare benefits, you are quite fortunate.

Employers also contribute to Provident Fund

As we know, employee’s contributions to the fund will be deducted between 2%-15% from employee’s monthly salary. As well as employer’s contributions to the fund which contribution rate will be depending on the company’s policy. In general, the longer "period of employment", the more you will contribute to the provident fund. It is not wrong to say that employees are profit from the beginning since the employer helps save money as well.

Contribution to Provident Fund is tax deductible

The accumulated money that employees contribute to the provident fund every month is tax deductible. However, when combined with Super Savings Fund (SSF), Annuity Insurance, Retirement Fund (RMF), National Savings Fund (NSF), Pension Fund, Government Pension Fund (GFP) and Private Teacher Aid Fund, the total accumulated amount of all the fund mentioned above that can be tax deductible must not exceed 500,000 Baht.

In order to encourage employees to continue saving money for their retirement. The law therefore requires the retired age of the fund member must be 55 years old and has been a member of the provident fund for at least 5 years in order to fully received tax benefit. But if the fund members quit the job with less than 5 years’ period of employment, fund management company has a duty to deduct withholding tax of provident fund income before the member receives the money and report to the Revenue Department immediately. Thus, the members who receive money from the provident fund under any circumstances has a duty to report the Revenue Department of this amount of income when submitting personal income tax as well. In conclusion, if fund members are able to contribute to the fund until the age of 55, members will receive the most benefit of their contributions.

A wide range of investment types, both domestically and internationally for Provident fund are allowed.

นอกจากนี้การเลือกลงทุนผ่านกองทุนสำรองเลี้ยงชีพ เรายังสามารถเลือกลงทุนได้ตามความต้องการของเรา ใครชอบเสี่ยงน้อยก็สามารถเลือกลงทุนผ่าน "ตราสารหนี้" และเลือกลงทุน "ตราสารทุน" ที่น้อยลงได้ แต่ถ้าใครชื่นชอบความเสี่ยงและอยากกระจายการลงทุนไปในต่างประเทศ กองทุนสำรองเลี้ยงชีพก็มีนโยบายที่ให้เราสามารถเลือกแหล่งการลงทุนได้ด้วยตัวเองด้วย

How much money should the fund member contribute to provident fund?

In general, the more contributions, the more benefits to the fund member. This is because the fund members are allowed to decide how much they want to contribute into the fund each year to be tax deductible. This also increase chances that employees will retire with quality. Nevertheless, for anyone who wants to know how much money they should contribute into the provident fund, it will be neither too much nor too small.

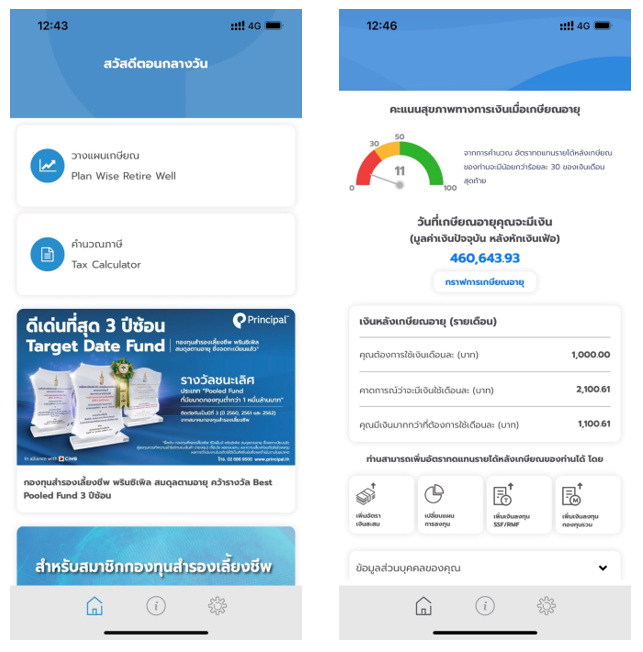

Principal Asset Management utterly understands the needs of fund members. So, we have provided provident fund application, Principal PVD which can be easily downloaded to your mobile phone. You can try planning your retirement whether you are a provident fund member or not by opening the application and fill out your information. Then, clicking into “Plan Wise Retire Well”, the application will ask you to provide the rate of your contributions to the provident fund. You can also include return on investment rate in your selected retirement plan for the application to calculate the expected amount money you will be getting on your retirement date. This will be useful for everyone who needs help on retirement planning.

After filling out your information, the application will help you see the whole picture of your retirement plan clearly. The information which required by the application are;

1. Age

2. Expected retirement age

3. Expected life expectancy

4. Salary

5. Salary growth rate

6. Contribution rate to provident fund

7. Expected return on investment

8. Other retirement funds and how much amount are they

9. Amount of money required after retirement per month

When you completely fill out these information, the application will calculate and suggest what you should do with your retirement plan. For those who are able to retire as intended can continue following the plan. But for those who has not been able to retire as intended, you may have to reconsider the contribution rate, invest more in other retirement funds or even changing the investment plans that offer greater expected returns.

For fund member who wishes to modify the investment plan but do not have time to follow up or have not much investment knowledge, we recommend you to invest through “Principal Target Date Retirement Fund” which is designed to help fund member to enjoy investment more while their investment capital will be managed closely by fund manager. Another option, “Principal Target Risk Fund” for employees who already plan out their retirement. Employees are allowed to allocate their investment assets and select their investment portions including investment in risky assets in do-it-yourself policy.

Disclaimer: Investors should understand the product type (fund), conditions, returns, and risk before deciding to invest / Previous performance could not guarantee for future performance

More information: https://www.principal.th/en/ or 02-686-9595

Follow Principal Thailand :

Facebook : https://www.facebook.com/principalthailand

LINE : https://lin.ee/C6KFF6E or @principalthailand

YouTube : https://www.youtube.com/channel/UCqELMp69UteyKgtWo4JuBqg

Disclaimer:

Investors should understand product characteristics (mutual funds), conditions of return and risk before making an investment decision / Past performance of the fund is not a guarantee for future performance / Plan WISE Retire WELL is only an investment model to study the possibility of expected return only. It is not a guarantee of future returns.