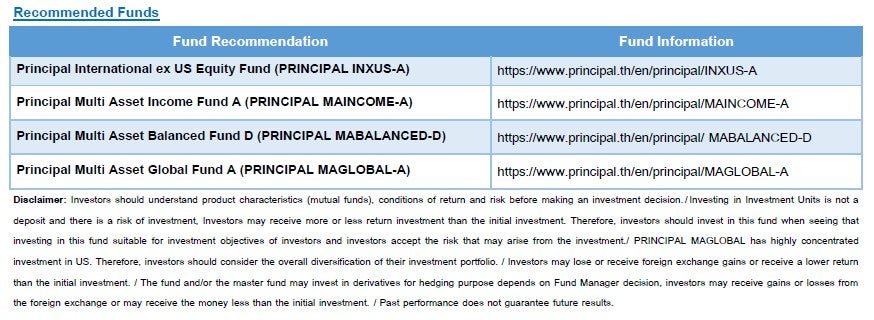

CIO View: February 2026

Image

Global markets enter March navigating a complex crosscurrent of political transitions, diverging central‑bank paths, and early signs that 2026 may represent a meaningful shift from the choppy macro backdrop of 2025. Shifts in monetary leadership—particularly in the United States and Japan—are emerging just as inflationary pressures moderate and fiscal expansion gains momentum across key economies. This combination of changing policymakers, uneven growth dynamics, and recalibrated expectations suggests that policy direction may again become the primary driver of asset performance rather than macro fundamentals alone.

In the United States, the nomination of Kevin Warsh to succeed Jerome Powell has introduced a new layer of uncertainty to the monetary‑policy outlook. Warsh, once known for his hawkish stance, now signals a pragmatic shift toward lower interest rates and greater policy flexibility, aligning with President Trump’s preference for a more accommodative stance. His belief that AI‑driven productivity gains can support faster growth without igniting inflation underpins his proposal for an unconventional mix of rate cuts alongside continued quantitative tightening. This comes as the January FOMC minutes reveal a committee increasingly uneasy with easing too quickly, noting that several members see limited justification for further cuts until inflation shows clearer progress toward 2%, and a minority even warned that rate hikes remain a possible response to stronger‑than‑expected data. Those concerns were reinforced by the January jobs report, which showed a sharp rebound in hiring to 130,000—well above expectations and sharply contrasting with the substantial downward revisions to 2025 job creation.

Amid these developments, the policy backdrop was further complicated by a recent U.S. Supreme Court ruling. On February 20, 2026, the Court ruled 6–3 that the International Emergency Economic Powers Act (IEEPA) does not authorize the imposition of tariffs, noting that the statute contains no reference to duties and cannot substitute for explicit congressional authorization. The decision invalidated the previous 10% global tariff and a range of higher country‑specific duties imposed under earlier executive actions. In response, President Trump signaled his intention to restore similar measures through alternative legal authorities, first announcing a new 10% global tariff under Section 122, and then shortly afterward threatening to raise the rate to 15%. However, official documentation indicates that the tariff currently in effect remains at 10%, with no directive yet issued to implement the higher rate. While the market implications remain uncertain, the episode underscores the fluidity and unpredictability of the legal environment surrounding U.S. trade policy.

Across Europe and China, monetary decisions are similarly stable but driven by distinct sets of risks. The ECB maintained a steady stance at its February meeting, keeping rates unchanged while highlighting that although inflation fell to 1.7% in January, the path ahead may still be uneven. President Lagarde reiterated a data‑dependent, meeting‑by‑meeting posture and pushed back against expectations of an imminent March cut. Meanwhile, the PBOC also kept its Loan Prime Rates on hold for a ninth consecutive month, signaling a cautious approach that balances the need for support with concerns about currency stability and bank margins, particularly in the post–Lunar New Year period. While both central banks are avoiding premature easing, the underlying drivers—low inflation stability in Europe versus financial‑stability considerations in China—differ considerably

The political landscape in Asia is shifting toward a stronger focus on aggressive fiscal policy, and Japan’s recent snap election is a key example of this trend. Sanae Takaichi’s landslide victory gave the Liberal Democratic Party (LDP) a supermajority in the Lower House, providing the political stability needed to implement fiscal measures more freely. One of her major proposals during the dissolution of parliament was a temporary reduction in the sales tax on food to ease household living costs, reflecting the government’s preference for fast and direct fiscal support as Japan continues to face inflationary pressures. At the same time, the government is accelerating long‑term strategic investments in industries such as AI, semiconductors, quantum computing, and shipbuilding. With both political stability and an assertive fiscal stance, Japan is entering a phase where the government can push forward short‑term stimulus and long‑term economic capacity building at the same time.

A similar emphasis on fiscal activation is emerging in Thailand, where the Bhumjaithai Party’s clear election victory positions Prime Minister Anutin Charnvirakul to advance the “Economy 10 Plus” plan. The program aims to lift GDP growth above 3% by combining targeted cost‑of‑living measures with investments in technology adoption, SME competitiveness, EV‑oriented industrial ecosystems, and secondary‑city tourism development.

Monetary policy developments in Thailand added another layer to the domestic macro landscape. On 25 February 2026, the Bank of Thailand’s Monetary Policy Committee (MPC) delivered a surprise 4–2 decision to cut the policy rate by 25 basis points, lowering it from 1.25% to 1.00% with immediate effect. Markets had broadly expected the Committee to keep the rate unchanged going into the meeting, making the easing move more dovish than anticipated. The MPC cited a growth outlook that remains below potential through 2026–27, driven by structural impediments and intensified competition, alongside increasing downside risks to inflation due to lower energy prices, potential additional government measures, and limited demand‑side pressures. Credit conditions remain tight, the baht has appreciated, and SME and household liquidity remains constrained. While the majority viewed a rate cut as necessary to maintain supportive financial conditions and ease debt burdens, two members favored holding the rate at 1.25%, noting that previous easing was still working through the economy. The Committee also highlighted that monetary policy alone cannot address Thailand’s structural growth challenges, calling for broader reforms to enhance productivity and competitiveness.

Thailand’s recent economic data reflect this mixed yet improving environment. The economy expanded 2.5% year‑on‑year in the final quarter of 2025, accelerating sharply from 1.2% in Q3 and exceeding government expectations. The surge was fueled by an 8.1% rise in total investment and solid private consumption, amplified by automotive purchases ahead of the expiration of EV 3.0 subsidies. Full‑year growth reached 2.4%, outperforming the government’s initial 2.0% projection. Yet the resilience was not uniform: tourism‑related services contracted 6.9% in Q4, and agriculture posted only marginal gains as global price competition continued to weigh on key crops. Nevertheless, the NESDC’s upgraded 2026 growth forecast of 1.5%–2.5% reflects growing confidence that a new government and targeted fiscal measures will help stabilize momentum.

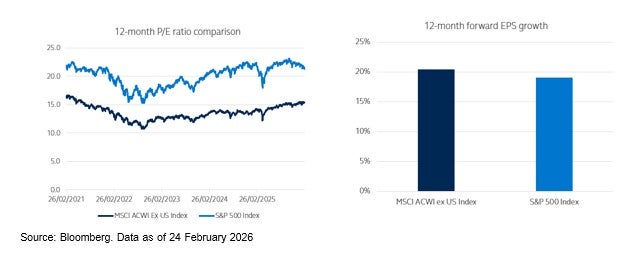

Against this backdrop of diverging macro trends, evolving policy regimes, and shifting political landscapes, a compelling opportunity continues to emerge in Global ex‑US equities. Investors worldwide are increasingly reassessing the degree of U.S. concentration embedded in their portfolios. Many global benchmarks allocate nearly two‑thirds of their equity exposure to the U.S., while thematic and growth‑oriented portfolios often push effective U.S. weights toward 70–90 percent. Relative valuations, however, remain meaningfully more attractive outside the United States. As of 24 February 2026, the MSCI ACWI ex USA traded at a forward P/E of roughly 15.4x—materially lower than the S&P 500’s 21.5x. At the same time, earnings expectations are broadly similar: Bloomberg and major sell‑side forecasts call for 20.5% earnings growth across non‑U.S. markets over the next year, compared with around 19.1 percent for the S&P 500.

Image

What distinguishes Global ex‑US markets is the breadth of their expected recovery. Europe, the UK, Asia ex‑Japan, China, and emerging markets all show prospects for double‑digit earnings expansion, supported by improving global demand, investment cycles, and increasingly stable currency conditions. Sentiment and positioning have also turned more constructive, with late‑2025 fund‑flow data indicating renewed interest in international equities and early signs of diversification away from U.S.‑centric exposures. Several 2026 market outlooks highlight this global rebalancing as a recurring theme.

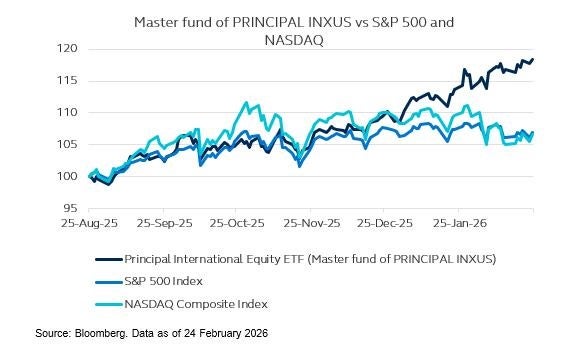

For investors looking to capture this opportunity while managing concentration risk, the Principal International ex US Equity Fund (PRINCIPAL INXUS) offers a timely and targeted way to access Global ex‑US opportunities. The fund was launched during its IPO period from 9–20 February 2026 and reopened on 4 March 2026. It invests in the Principal International Equity ETF as its master fund and employs an active, high-conviction investment approach across both developed and emerging markets. Its strategy blends growth and value exposures, anchored by free‑cash‑flow analysis and a disciplined search for companies whose cash‑generation potential is underappreciated. As of 24 February 2026, the master fund has delivered strong performance: 38.3 percent over one year, and an annualized return of 33.9 percent since inception. This compares with its benchmark, the MSCI ACWI ex US Net Total Return Index, which recorded returns of 35.5 percent over one year and an annualized return of 30.1 percent since inception.

Given comparable earnings growth, materially cheaper valuations, broader regional performance drivers, and improving global flow dynamics, increasing exposure to Global ex‑US equities remains a compelling allocation strategy. PRINCIPAL INXUS provides an effective and focused vehicle for implementing this shift in the current environment.

Image

Image