CIO View: June 2026

Image

Global financial markets in June 2026 were characterized by heightened volatility and a corrective phase, as investors reassessed risk in response to rising bond yields and increasingly stretched equity valuations—particularly within technology and AI related sectors. The repricing of interest rate expectations, supported by resilient macroeconomic data and more hawkish signals from major central banks, drove a broad-based increase in sovereign yields. This dynamic exerted pressure on long-duration assets and triggered a rotation away from mega cap growth stocks that had previously led market performance.

U.S. technology indices, particularly the Nasdaq and semiconductor stocks, recorded notable declines as investors questioned the sustainability of elevated earnings expectations and valuation multiples following the strong AI driven rally earlier in the year. While overall corporate earnings momentum remains constructive, market breadth has narrowed further. Performance has become increasingly sensitive to shifts in interest rates and investor sentiment, underscoring the fragility of current equity valuations.

Macro Backdrop: Resilient Growth, Persistent Inflation

In the United States, recent macroeconomic data points to a complex policy environment where resilient growth coexists with persistent inflationary pressures. Headline CPI accelerated to 4.2% year on year in May—its highest level in three years—largely driven by energy prices, while core inflation remained comparatively contained at 2.9%. Meanwhile, labor market conditions continue to show strength, with stable unemployment and sustained job creation.

This combination reinforces a cautious Federal Reserve stance. At the June 16–17 FOMC meeting—Chair Kevin Warsh’s first—the Fed held its policy rate unchanged at 3.50%–3.75% but adopted a more hawkish bias, emphasizing that inflation remains above target and removing prior forward guidance for rate cuts. Updated projections signal higher inflation expectations, modestly weaker growth, and a stable labor outlook. Notably, the median rate path now implies at least one additional hike in 2026, reflecting concerns around inflation persistence.

Beyond policy direction, the Fed also introduced adjustments to its communication approach, including reduced reliance on explicit forward guidance and a broader review of its policy framework—signaling a shift toward greater flexibility and optionality in how policy is communicated amid an uncertain macro backdrop.

Global Policy Landscape: Divergence with a Hawkish Tilt

Across other developed markets, the policy backdrop remains uneven, with central banks responding to differing domestic conditions rather than moving along a synchronized normalization path. The European Central Bank raised its deposit rate by 25bps to 2.25%, marking its first hike since 2023, as persistent energy driven inflation offsets weakening growth. Updated ECB projections point to a more stagflationary mix, with inflation near 3.0% and GDP growth subdued at around 0.8% for 2026.

In Japan, the Bank of Japan raised its policy rate to 1.00%—its highest level since 1995—continuing its gradual shift away from ultra accommodative policy as wage growth and inflation dynamics improve. Both central banks emphasize a cautious, data dependent approach, reflecting the delicate balance between inflation risks and slowing growth.

In contrast, China maintains an accommodative stance. The People’s Bank of China kept benchmark lending rates unchanged, focusing instead on liquidity management and targeted structural measures to support domestic demand amid mixed economic momentum and ongoing external uncertainties.

Geopolitics: Temporary Relief, Structural Risks Remain

Geopolitical developments continue to shape the macro and market backdrop. The mid June agreement between the United States and Iran represents a temporary de escalation, including a ceasefire framework, the reopening of the Strait of Hormuz, and a partial resumption of Iranian oil exports. While this has helped stabilize near term energy supply expectations, the agreement remains provisional, with key issues unresolved and subject to further negotiations.

As such, geopolitical risks remain elevated, particularly in relation to energy markets and inflation, contributing to continued uncertainty across asset classes.

Thailand: Policy Stability Amid Uneven Recovery

Thailand’s economic recovery remains modest and uneven. The Bank of Thailand has maintained its policy rate at 1.00%, supporting growth while monitoring inflation risks. GDP is projected at 2.3% in 2026 and 1.8% in 2027, supported by exports, targeted fiscal measures, and technology related investment.

Inflation is expected to temporarily rise above target in 2026 before moderating, while financial conditions remain broadly stable. However, credit growth remains uneven, particularly among SMEs, and vulnerabilities persist within lower‑income segments. The Thai baht has depreciated alongside broader U.S. dollar strength.

From a policy perspective, the window for further rate cuts appears to have narrowed meaningfully, while the case for rate hikes remains limited. The expected inflation uptick is likely to be temporary, particularly given recent easing in geopolitical tensions and energy price risks. As a result, the Bank of Thailand is likely to remain on hold, maintaining a data dependent stance while balancing growth support and financial stability considerations.

Investment Strategy: Resilience in an Uncertain Regime

In an environment defined by shifting macro conditions, elevated volatility, and uncertain policy trajectories, portfolio construction must prioritize resilience, diversification, and flexibility. Multi asset strategies are well positioned to navigate such conditions, offering diversified return streams across asset classes and market environments.

We continue to advocate an “all weather” approach, emphasizing adaptability and disciplined risk management. This framework allows portfolios to remain robust across a wide range of macro outcomes, from persistent inflation to slower growth.

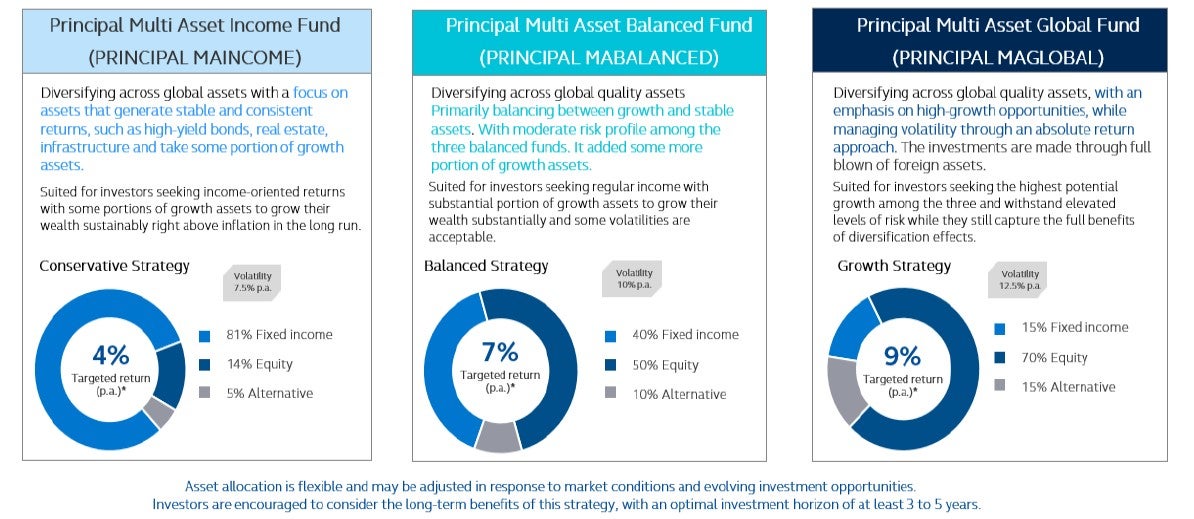

Preferred Multi-Asset Solutions

• PRINCIPAL MABALANCED: Balanced allocation between equities and fixed income, designed to manage volatility while delivering steady returns

• PRINCIPAL MAINCOME: Income oriented strategy with higher fixed income exposure, suitable for conservative investors

• PRINCIPAL MAGLOBAL: Growth tilted allocation with higher equity exposure, suited to investors with longer time horizons and higher risk tolerance

Image

*The reference benchmark of the PRINCIPAL MAINCOME Fund consists of MTMGov 0–1Yrs NTR Index (67%), SDHY LN (14%), and WORLDN Index (14%). The reference benchmark of the PRINCIPAL MABALANCED Fund consists of WORLDN Index (50%), MTMGov 0–1Yrs NTR Index (30%), SDHY LN (10%), and SOFRINDX Index (10%). The reference benchmark of the PRINCIPAL MAGLOBAL Fund consists of WORLDN Index (70%), BIL US (15%), and SOFRINDX Index (15%). The figures presented above are calculated based on the historical performance of each fund’s benchmark over a 10-year period from 2015 to 2025, resulting in average annual returns of approximately 4%, 7%, and 9%, respectively. These returns are for historical reference only and do not constitute a guarantee, estimate, or confirmation of future performance. Source: ThaiBMA and Bloomberg.

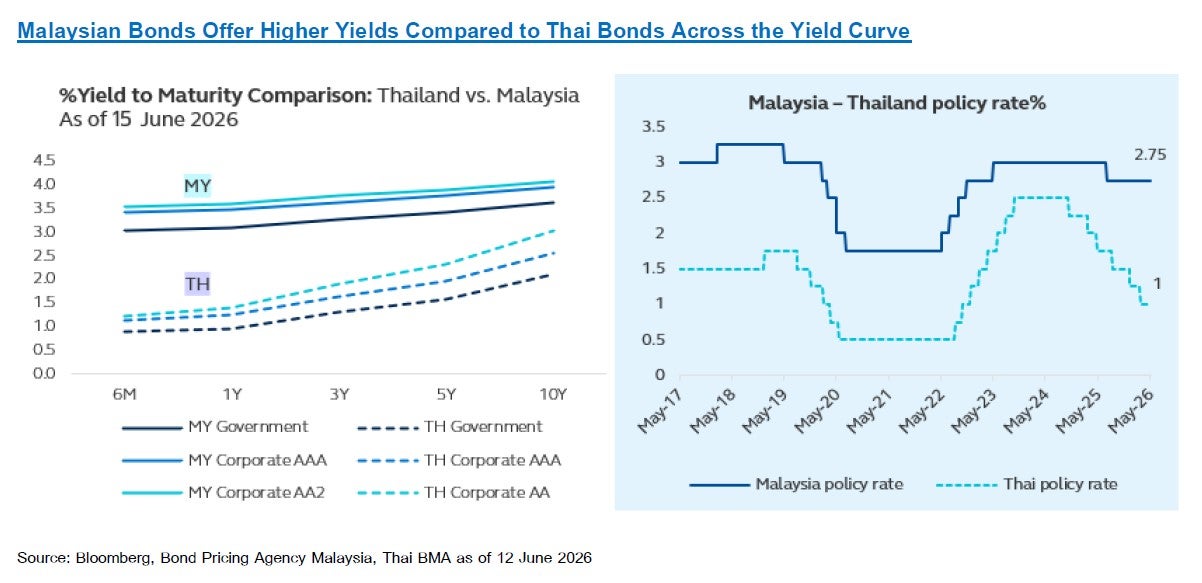

Fixed Income Opportunity: Malaysia’s Relative Strength

Beyond multi asset strategies, Malaysian fixed income presents a compelling opportunity within the region. The Principal Malaysian

Fixed Income Fund Unhedged (PRINCIPAL MYRFIUH) offers exposure to an economy supported by resilient domestic demand and solid external balances, with GDP growth expected to remain healthy into 2026.

Malaysian Government Securities (MGS) and high quality corporate bonds continue to offer attractive yield carry relative to Thai bonds, supported by credible fiscal management and a stable policy outlook.

Importantly, Malaysia’s position as ASEAN’s only net energy exporter provides a structural advantage during periods of elevated oil prices, supporting fiscal stability and currency resilience. This contrasts with Thailand, where sustained high energy prices could weigh on fiscal balances through subsidy mechanisms and increase macro vulnerability.

As a result, Malaysia’s relative macro strength and external position may help support MYR versus THB over time, reinforcing the attractiveness of MYR denominated fixed income exposure.

Image

Conclusion

Market volatility is likely to remain elevated as inflation risks persist, growth moderates, and policy expectations continue to evolve. At the same time, equity valuations in certain high growth segments—particularly AI and semiconductor related sectors—appear increasingly sensitive, with pockets of both stretched valuations and earnings expectations that may prove difficult to sustain. Positioning in these areas also appears relatively crowded, increasing the risk of sharper corrections.

In this environment, a diversified, flexible, and disciplined investment approach is essential. An all weather multi asset framework—complemented by selective fixed income opportunities—remains a robust strategy to navigate uncertainty while preserving long term return potential.

Image

Disclaimer: Investors should understand the characteristics of the product (mutual fund), conditions, returns, and risks before making an investment decision. Investment in mutual fund units is not a deposit and carries investment risks. Investors may receive a return that is higher or lower than the initial investment. Therefore, investors should invest in this fund when seeing that investing in this fund suitable for investment objectives of investors and investors accept the risk that may arise from the investment. PRINCIPAL MAGLOBAL has a concentrated investment in the United States. Investors should consider diversifying the overall risk of their investment portfolio. The fund invests in foreign assets and may be exposed to foreign exchange (FX) risk. Investors may incur gains or losses from exchange rate fluctuations and may receive proceeds lower than the initial investment. The management company may use derivatives as a tool for hedging exchange rate risk at its discretion. The fund adopts a dynamic hedging policy (0%–105% of exposure). PRINCIPAL MYRFIUH has a concentrated investment in Malaysia. Investors should consider diversifying the overall risk of their portfolio. The fund invests in foreign assets and is subject to foreign exchange risk, which may result in gains or losses or returns lower than the initial investment. PRINCIPAL MYFIUH does not hedge foreign exchange risk (unhedged). Therefore, investors are fully exposed to FX risk, which may result in losses or proceeds lower than the initial investment. Past performance is not indicative of future results.