CIO View: March 2026

Image

This CIO View approaches the ongoing Middle East conflict strictly through the lens of investment risk management rather than geopolitics. As a CIO, my role is not to interpret political developments or forecast how the conflict may evolve, but to help investors navigate uncertainty with a disciplined, all weather approach. The scenarios presented in this paper are not geopolitical predictions. They are analytical tools designed to frame potential macro and market implications across different paths of disruption, enabling investors to assess risks methodically rather than speculate on outcomes. This is not a trading call or a political view. For formal geopolitical analysis, readers should refer to insights published by Principal Asset Management’s Global Insights team, led by Seema Shah, Chief Global Strategist. With this risk management foundation in place, we now turn to the market dynamics shaping the months ahead.

The escalation of the Iran conflict in late February and March 2026 has triggered the largest disruption to global oil supply in modern history, sending energy markets into turmoil and elevating uncertainty across financial markets. With the Strait of Hormuz through which roughly one‑fifth of the world’s crude oil and LNG normally transit effectively shut due to escalating attacks and widespread security risks, global oil flows have fallen to almost nothing prompting Brent crude to surge past USD 100 per barrel and fueling sharp increases in gasoline, diesel, and transportation costs worldwide.

The supply shock has forced major producers to cut shipments, prompted the International Energy Agency (IEA) to authorize a record emergency stockpile release, and exposed deep vulnerabilities for import‑reliant regions, particularly in Asia, where governments are rationing energy and curbing industrial activity. Against this backdrop of heightened geopolitical risk, elevated energy prices, and tightening global financial conditions, investors face an environment marked by volatility and persistent uncertainty setting the stage for strategies that prioritize diversification and resilience.

Amid the turmoil from the Iran conflict and the surge in oil prices, major central banks took a cautious stance post their meeting in March, with the U.S. Federal Reserve, European Central Bank, and Bank of Japan all choosing to keep interest rates unchanged as they assessed the inflationary shock caused by soaring energy costs. The Fed held rates at 3.50%–3.75%, noting that higher oil prices add uncertainty to the inflation outlook, even as recent economic data continues to indicate resilience, leading investors to scale back expectations of near‑term rate cuts. The ECB likewise kept policy steady, noting that the Middle East conflict is now pushing energy prices higher and likely slowing growth, reinforcing the need for caution. Meanwhile, the BOJ faced renewed pressure as the yen hovered near a two‑year low following the Fed’s decision, reflecting concerns about policy divergence and rising oil‑related inflation risks. Across global markets, the sharp jump in oil prices has clearly shifted expectations: what had been a widely anticipated path of steady rate cuts earlier in the year has now given way to a “higher for longer” outlook, with some markets even beginning to price in the possibility of future rate hikes in the UK and eurozone if energy‑driven inflation persists. Meanwhile, the PBOC reaffirmed a moderately accommodative policy bias, emphasizing liquidity support, financial market stability, and targeted measures rather than headline rate changes to underpin growth.

While policy responses provide an early indication of how authorities are assessing the shock, the broader economic impact will depend on how long energy market disruptions persist. To frame the potential range of outcomes, it is helpful to turn to quantitative sensitivity models that estimate how sustained oil price increases could affect growth and inflation across major economies.

According to guidelines from a Federal Reserve model, oil price shocks can serve as a useful reference point for understanding how the economy might react in the months ahead. Historically, a USD 10 per‑barrel rise in crude oil is associated with a roughly 0.1 percentage‑point drag on U.S. GDP growth and about a 0.3 percentage‑point increase in headline inflation over the following year, though the model emphasizes that these effects become far less predictable at higher price levels. These pressures could also extend well beyond energy, given the Middle East’s critical role in global fertilizer supplies and helium used in semiconductor manufacturing, meaning that a more prolonged conflict could have broader implications for both growth and production costs. With so much uncertainty around how long the disruption will last and how quickly energy flows might normalize, the range of potential economic outcomes has widened considerably.

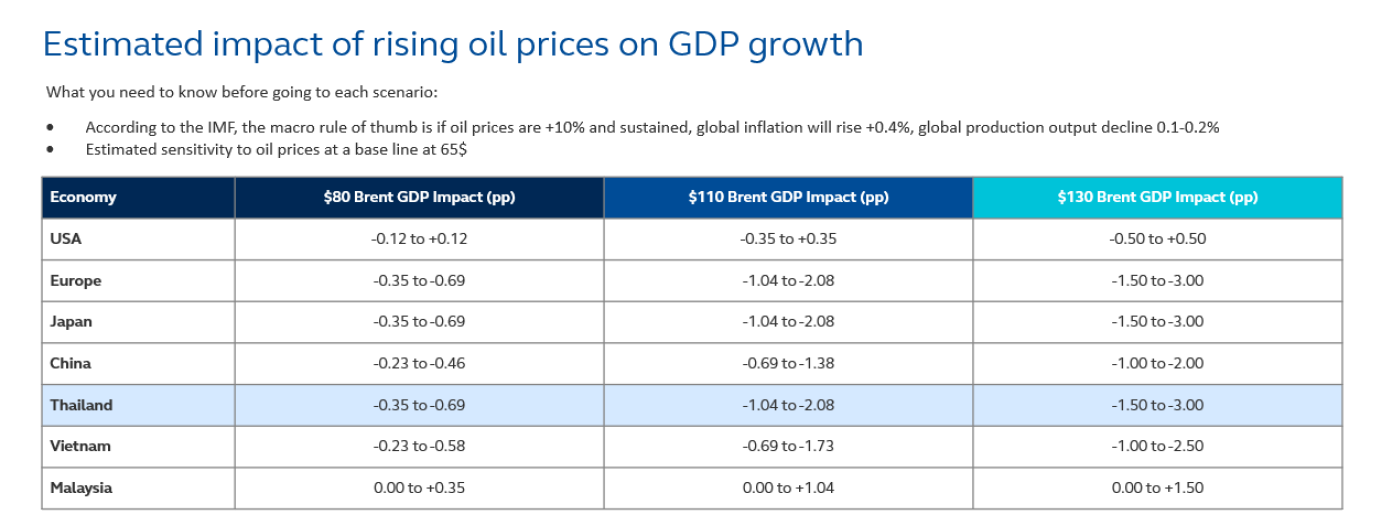

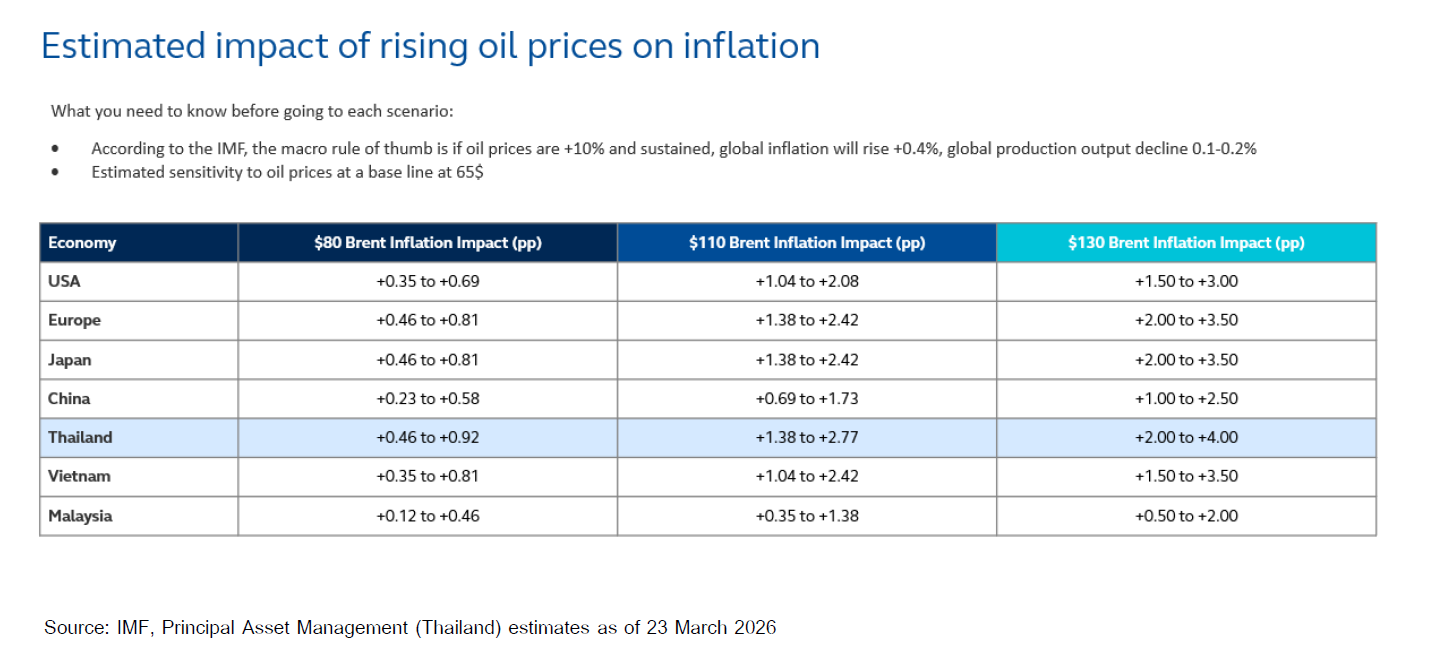

Beyond the Federal Reserve’s estimates, the IMF’s sensitivity framework provides a clearer picture of how prolonged oil price spikes could impact the global economy. Using a baseline Brent crude price of USD 65 per barrel, the IMF estimates that every sustained USD 10–20 increase in oil prices can significantly push inflation higher and slow economic growth, especially in countries that rely heavily on imported energy. At USD 110 Brent, headline inflation across major regions could rise by +1.0 to +2.5 percentage points, and by +3.0 to +4.0 percentage points should prices reach USD 130. Emerging Asian economies such as Thailand, India, and Vietnam face some of the largest inflation pass‑through effects due to their higher dependence on imported crude.

The IMF model also shows that rising oil prices could reduce global GDP growth by –0.7 to –2.0 percentage points, with deeper contractions of –1.5 to –3.0 percentage points in more oil‑sensitive markets if Brent rises to USD 130. These simultaneous inflation‑and‑growth pressures highlight rising stagflation risks particularly in Asia where elevated energy costs could weaken household spending and strain industrial output at a time when global demand is already softening. In a market where energy shocks heighten uncertainty and downside risks, investors need strategies that offer resilience, inflation protection, and flexibility. Multi‑asset funds are well‑positioned for this environment, dynamically adjusting allocations and incorporating global macro insights such as energy‑price sensitivities and regional risk exposures, to help manage volatility. For investors seeking to navigate potential stagflation while staying positioned for long‑term growth, a multi‑asset approach provides an effective and timely solution. These model sensitivities reinforce the importance of building portfolios capable of navigating shifting inflation dynamics—a core principle of an all-weather investment approach.

Image

Image

Scenario Analysis: Mapping Potential Paths of the Conflict and Market Implications

Given the uncertainty surrounding the duration and scale of the disruption to energy transit routes, we outline three potential scenarios—Quick End, Moderate End, and Prolonged Conflict—to frame how different outcomes could influence global markets and the Thai economy. These scenarios are designed to help investors calibrate positioning under varying assumptions about energy supply normalization, inflation pressures, and external demand conditions.

Scenario 1: Quick End (Resolved Within Three Months)

A rapid easing of regional tensions would represent a short lived volatility shock, allowing supply routes through the Strait of Hormuz to gradually reopen and stabilizing energy markets. Global equities would likely experience a relief rebound as inflation pressures subside. Technology, consumer discretionary, and other growth oriented sectors would be positioned to recover, while fixed income markets would stabilize alongside moderating inflation expectations.

Oil prices would likely retrace toward the USD 70–90 range as supply bottlenecks clear and emergency stockpiles are replenished. Safe haven demand for gold would soften, and REITs would benefit as financing conditions improve. For Thailand, the macro impact remains manageable: GDP growth may face a limited drag of –0.35 to –0.7 percentage points, while headline inflation would experience only a temporary rise before normalizing. Tourism losses would be contained, and the Bank of Thailand (BOT) would likely maintain an accommodative stance to support the recovery. In this scenario, market volatility subsides, and investors can tactically add risk in areas tied to energy normalization and domestic consumption recovery.

While this is the most benign scenario, it still underscores the value of maintaining diversified exposures that can adapt quickly as conditions normalize.

Scenario 2: Moderate End (Disruption Lasts 3–6 Months)

A more extended period of disruption would generate a measured slowdown as higher energy costs filter into core inflation and corporate margins. Oil prices stabilizing in the USD 90–120 range would keep inflation elevated for longer, prompting central banks globally to adopt cautious, data dependent approaches. Equity performance would become more dispersed, with energy, defense related industries, and income generating sectors outperforming, while energy intensive industries—including Airlines, Transport, and Chemicals—face sustained margin pressure. Demand for inflation linked instruments would increase as breakeven rates rise.

For Thailand, impacts would deepen. GDP could face a drag of –1 to –2 percentage points, driven by higher logistics costs, weaker export competitiveness, and softer global demand. Tourism could see a reduction of 1.5–2.0% of expected full year arrivals, while a sustained oil price near USD 100 would widen the trade deficit and place depreciation pressure on the Thai baht. The BOT would likely keep policy rates steady to support currency stability. In this environment, investors may prioritize resilience through selective exposure to defensives, high dividend names, inflation linked assets, and sectors benefiting from regional supply chain re routing.

This scenario shows the benefit of an all-weather framework, where defensive positioning and income strategies help manage rising volatility.

Scenario 3: Prolonged Conflict (Extends Beyond 2026)

A long lasting disruption would create a stagflation prone environment, with structurally higher energy prices, persistent supply chain realignment, and prolonged logistical constraints. Oil prices remaining above USD 120 would significantly raise global cost pressures, weighing on growth across both advanced and emerging economies. Global equities would likely shift toward defensive positioning, with Consumer Staples, Healthcare, and traditional Energy sectors providing relative resilience. Long duration fixed income would struggle to offer diversification benefits in a persistently high inflation environment, while commodities and short duration instruments gain importance.

For Thailand, the macro impact becomes severe. GDP could contract by –1.5 to –3.0 percentage points, particularly if elevated energy prices persist. Headline inflation could climb by more than +3 percentage points, adding pressure to household budgets and corporate margins. A widening current account deficit may result in sustained depreciation pressure on the baht, potentially compelling the BOT to tighten policy despite slowing growth. Key manufacturing segments—especially petrochemicals and packaging—would face material shortages, intensifying economic headwinds. In this scenario, investors would prioritize capital preservation, real assets, inflation hedges, cash flow resilient sectors, and currency risk management.

In a persistent stagflation environment, all-weather strategies that combine inflation protection, quality income, and disciplined risk management become critical.

Impact to Thai Fixed Income Across Scenarios

Thailand’s fixed income market reacts differently depending on the duration and severity of the energy shock, driven mainly by the BOT’s policy constraints, baht stability, and inflation pressure.

Quick End – Delay Cuts

• BOT Policy: Additional rate cuts remain possible if recovery needs support.

• Bond Yields: 10 year yields likely stabilize or edge lower as sentiment improves.

• Curve Impact: Mild flattening or range bound trading.

Moderate – Hold & Watch

• BOT Policy: Rate cuts delayed as baht depreciation becomes the key concern.

• Bond Yields: Yields drift higher across the curve as inflation stays elevated.

• Curve Impact: Bear flattening, with long end yields rising more than short end.

Prolonged – Forced Hike

• BOT Policy: Persistent high inflation and baht pressure could force rate hikes.

• Bond Yields: Significant upward shift across the curve.

• Curve Impact: High, sticky yields limit BOT’s ability to ease.

Impact to Thai Equity Across Scenarios

Thai equities respond strongly to changes in energy costs, currency movements, and tourism flows.

Quick End

• Market Reaction: SET likely rebounds quickly from early March volatility.

• Leaders: Airlines, Transport, and Chemicals lead the recovery.

• Index Level: Likely stabilizes above ~1,450.

Moderate

• Market Shape: “K shaped” performance emerges.

• Underperform: Consumer discretionary and exporters facing high logistics costs.

• Outperform: Banks, high dividend value names, and oil related stocks.

• Index Level: Trades sideways within 1,350–1,420.

Prolonged

• Macro Impact: High oil costs (≈6% of GDP import burden) lead to earnings downgrades.

• Sector Impact: Tourism weakens as higher travel costs hit demand.

• Index Level: Broad based correction with downside skew.

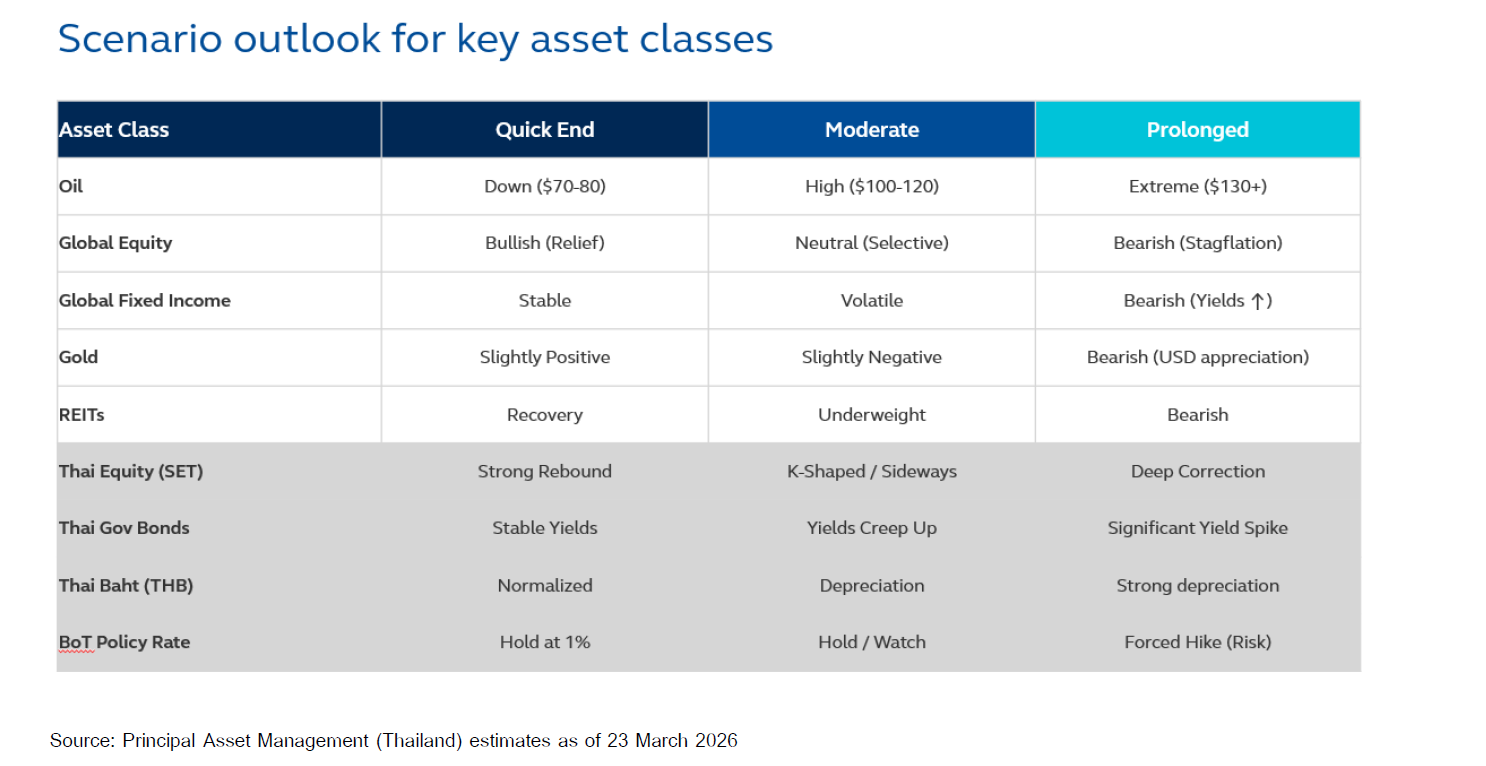

Summary of Cross Scenario Market Impacts

The table below provides a consolidated view of how selected asset markets could behave under the three scenarios outlined earlier. It is intended as a comparative stress scenario framework rather than a forecast, highlighting the relative direction and magnitude of potential moves across asset classes as the duration and intensity of the energy market disruption evolve.

Image

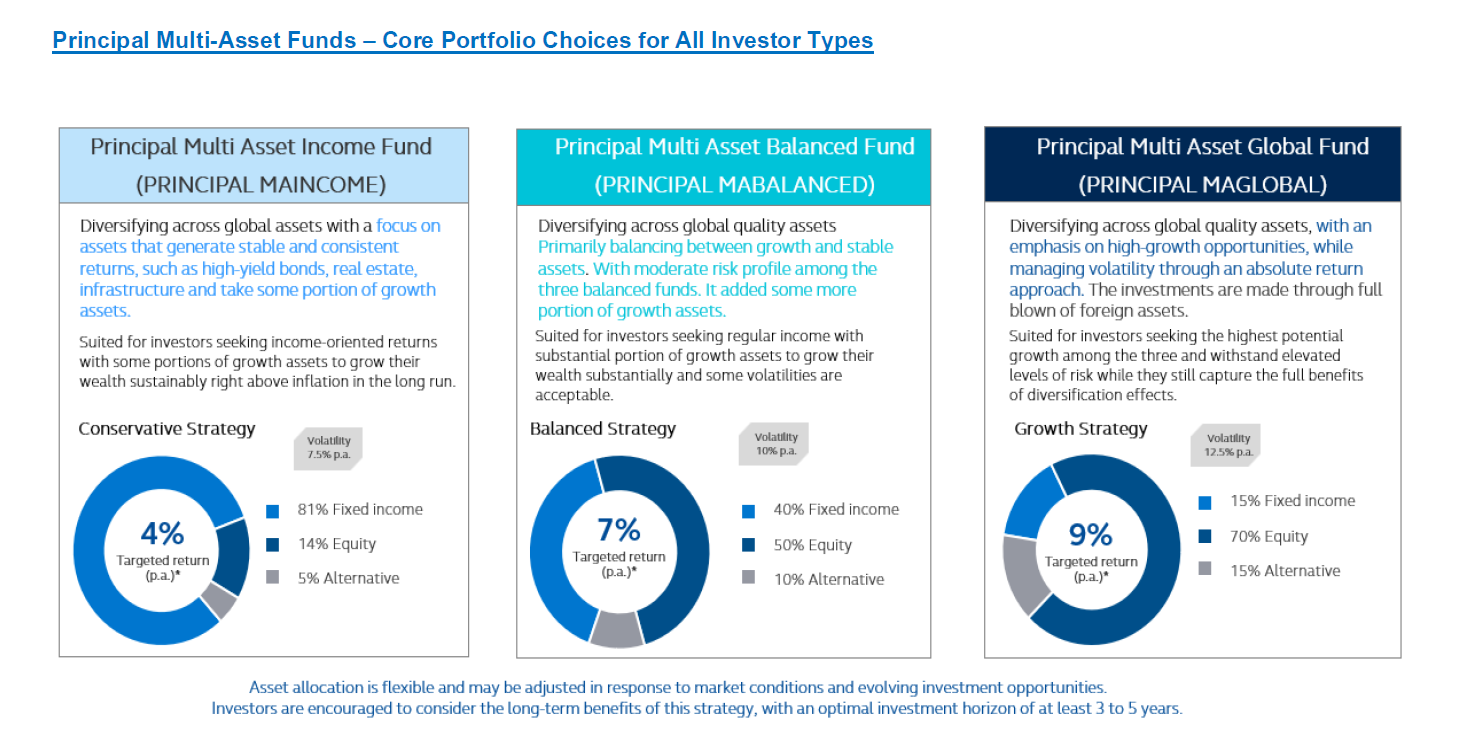

In an environment where macro conditions remain fluid, multi-asset strategies offer diversified engines of return that can help stabilize portfolios across varying economic regimes. Given the wide range of potential macro outcomes and the elevated volatility across asset classes, portfolio construction now needs to emphasize resilience, diversification, and adaptability—hallmarks of an all weather approach. The scenario analysis illustrates how market conditions may shift as energy disruptions evolve, but the common thread across all paths is the need for strategies that can withstand uncertainty while remaining positioned to capture opportunities as they emerge. With this in mind, we highlight a selection of multi asset and fixed income solutions structured to provide diversified exposures across different market conditions.

Market volatility is likely to stay high as inflation risks remain, growth slows, and interest rate expectations shift. In this environment, diversification and flexibility are key. Multi-asset funds can help by adjusting across different asset classes to manage risk and capture opportunity. Principal Multi Asset Balanced Fund (PRINCIPAL MABALANCED) provides a balanced allocation between equities and fixed income, helping manage volatility while targeting steady returns. Principal Multi Asset Income Fund (PRINCIPAL MAINCOME) leans more toward fixed income, making it suitable for conservative investors who want limited volatility and controlled downside risk. Principal Multi Asset Global Fund (PRINCIPAL MAGLOBAL) has higher exposure to growth assets, fitting investors who can accept more ups and downs in exchange for higher long-term growth potential. In addition, we recommend the Signature Global Dynamic Income Fund (SIGNATURE GINCOME) and the Signature Global Dynamic Income and Growth Fund (SIGNATURE GINGRO), exclusive solutions for CIMB clients designed to perform across market cycles. SIGNATURE GINCOME focuses on income generation, with a target of potential monthly payouts of 6% per annum in USD terms, achieved through investments in global fixed income, including investment-grade securities and yield-enhancing strategies, while SIGNATURE GINGRO aims to deliver both income and capital growth, with a target long-term total return of 8-10% per annum in USD and an income distribution of 4.0%-4.5% per annum in USD, investing in a globally diversified multi-asset portfolio. The IPO period is from 23 March to 3 April 2026.

In an environment defined by uncertainty—from geopolitical disruptions to shifting inflation dynamics—investors benefit most from strategies that can operate across multiple regimes. An all weather approach, grounded in diversification, disciplined risk management, and flexible asset allocation, remains one of the most effective ways to navigate market turbulence while preserving long term return potential.

Image

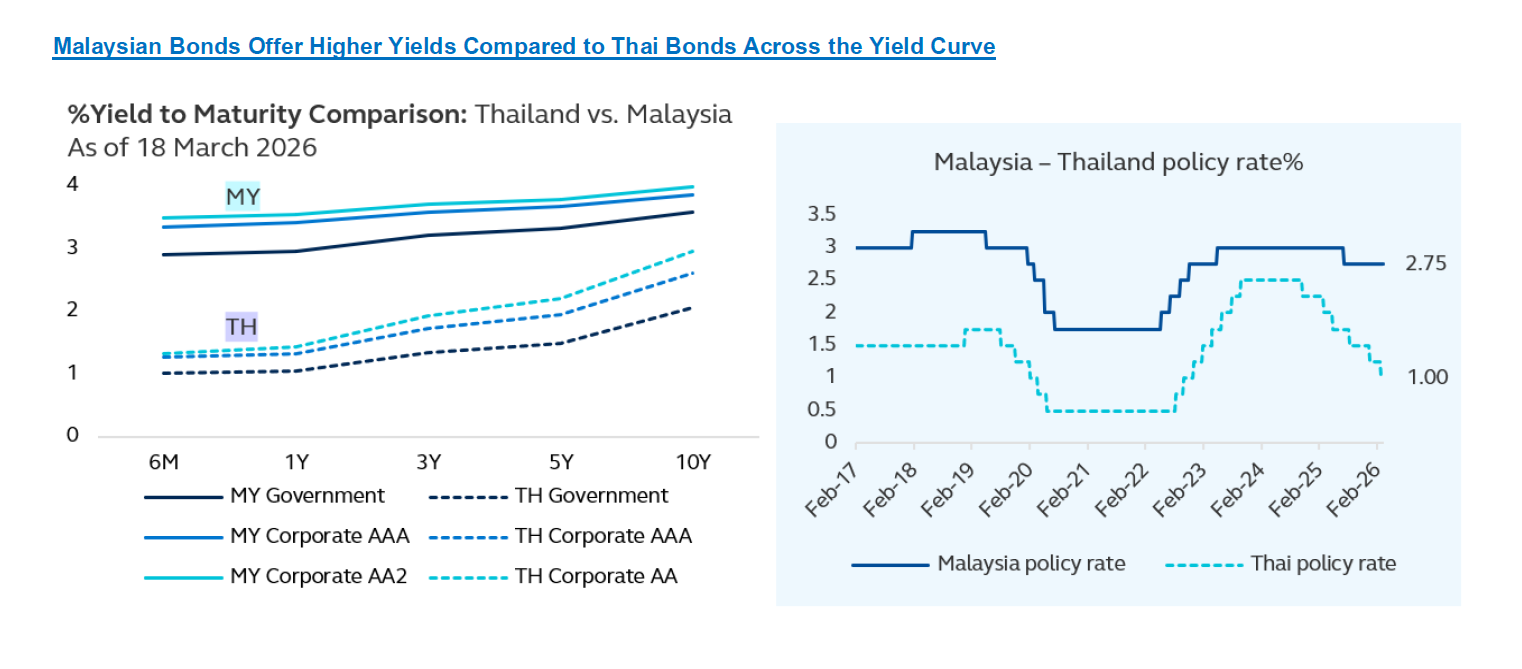

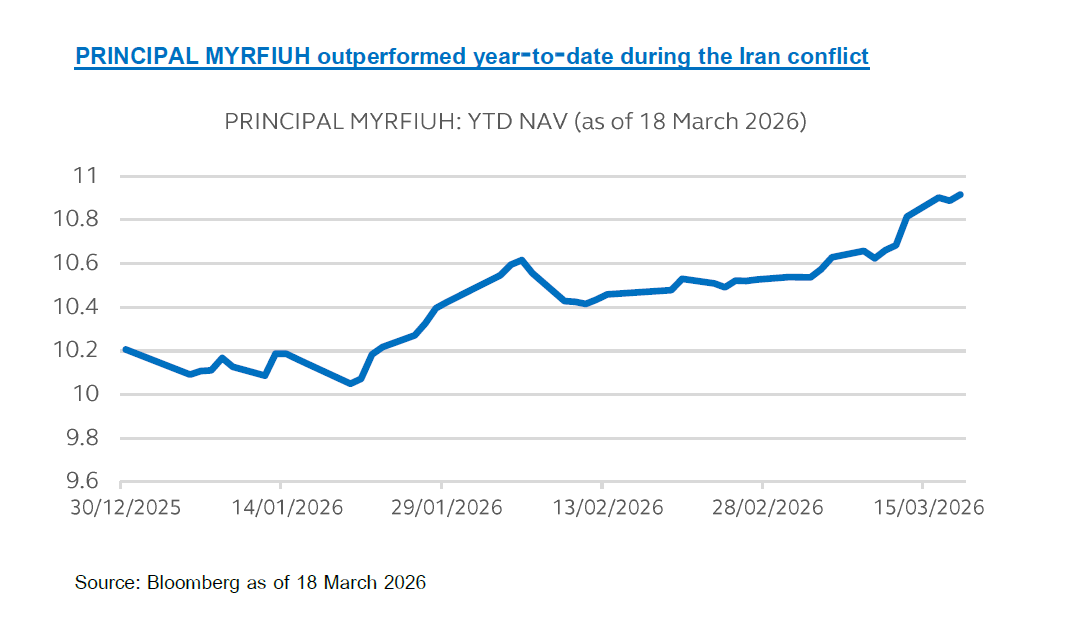

Beyond multi-asset strategies, we see value in adding the Principal Malaysian Fixed Income Fund Unhedged (PRINCIPAL MYRFIUH) to the portfolio. Malaysia’s economic fundamentals remain relatively resilient, supported by steady domestic demand and a solid GDP growth outlook of around 4.3% for 2026, according to the IMF. The country also benefits from strong external buffers, including LNG and palm oil exports, which continue to support its trade performance. From a fixed income perspective, Malaysian Government Securities (MGS) and high-quality corporate bonds offer a yield premium of approximately 1.8%–2.0% across most tenors. Combined with Malaysia’s credible fiscal management and stable policy outlook, this creates a favorable environment for bond investors.

Importantly, Malaysia is ASEAN’s only net energy exporter, giving it a meaningful buffer during periods of elevated oil prices, an advantage that enhances fiscal stability and supports MYR in times of global volatility. This stands in contrast to many regional peers that remain more exposed to energy‑price shocks. High oil prices remaining elevated increase Thailand’s fiscal risks, as subsidies through the Energy Stabilization Fund are likely to widen its deficit. This raise concerns over Thailand’s fiscal position and increases the risk of a sovereign credit rating downgrade. As a result, Thailand is relatively more vulnerable to prolonged high oil prices due to its energy importer status. Against this backdrop, Malaysia’s stronger energy position and more stable macro fundamentals may help support MYR relative to THB, reinforcing the attractiveness of MYR-denominated fixed income exposure through PRINCIPAL MYRFIUH. Overall, the combination of resilient economic growth, energy‑exporter advantages, and a strong fixed‑income yield environment makes PRINCIPAL MYRFIUH a compelling option for income‑seeking investors in today’s market.

Image

Image

Image

Disclaimer: Investors should understand product characteristics (mutual funds), conditions of return and risk before making an investment decision./Investing in Investment Units is not a deposit and there is a risk of investment, Investors may receive more or less return investment than the initial investment. Therefore, investors should invest in this fund when seeing that investing in this fund suitable for investment objectives of investors and investors accept the risk that may arise from the investment. PRINCIPAL MAGLOBAL, SIGNATURE GINGRO have highly concentrated investment in US. Therefore, investors should consider the overall diversification of their investment portfolio. PRINCIPAL MAGLOBAL, SIGNATURE GINGRO, and SIGNATURE GINCOME have a policy to invest in foreign investments. Investors may lose or receive foreign exchange gains or receive a lower return than the initial investment. The fund and/or the master fund may invest in derivatives for hedging purpose, at the discretion of the fund manager. The funds have a dynamic hedging policy, with a hedging ratio ranging from 0% to 105% of foreign exchange exposure. PRINCIPAL MYRFIUH has highly concentrated investment in Malaysia. Therefore, investors should consider the overall diversification of their investment portfolio. The fund has a policy to invest in foreign investments, and investors may incur losses or gains due to exchange rate fluctuations. PRINCIPAL MYRFIUH does not hedge against foreign exchange risk (unhedged). As a result, the fund is exposed to currency risk, which may cause investors to incur losses from exchange rate movements or receive less than their initial investment. Past performance does not guarantee future results.