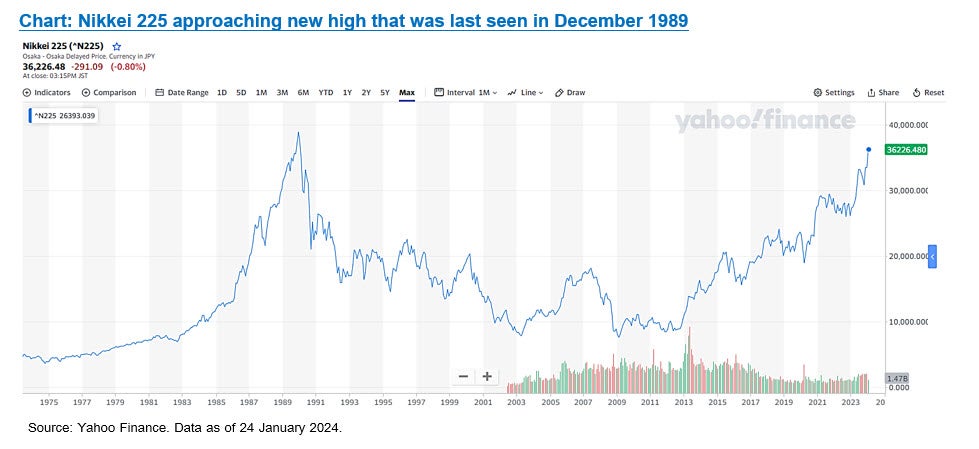

CIO View : January 2024 Japan – Party like it’s 1989!

Image

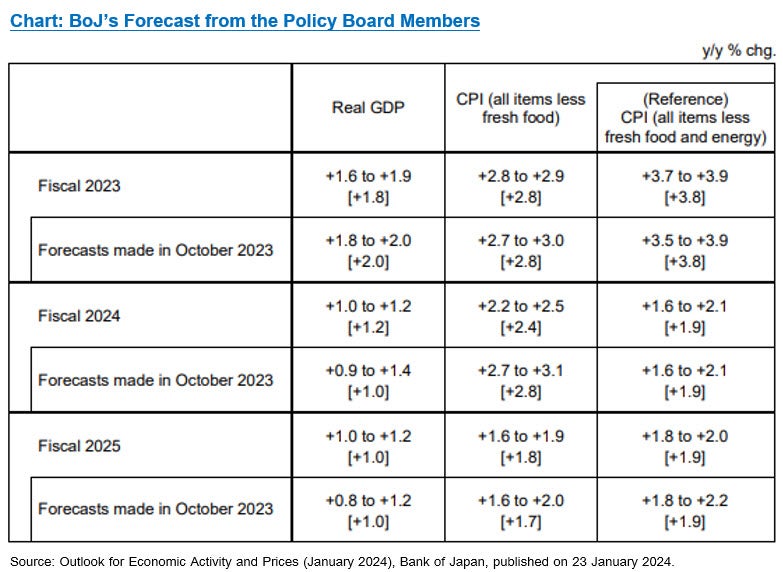

Bank of Japan held its Monetary Policy Meeting on January 22-23. For short-term interest rate, they maintained the negative interest rate of -0.1% for the balances held at the BoJ by financial institutions. For long-term interest rate, they maintained the purchase program for the 10-year Japanese government bond (JGB) by targeting the yield at 0%. And for the yield curve control, they maintained the upper bound of 1.0% for the 10-year JGB yields as a reference in its market operations. BoJ also maintained its purchase program for exchange traded funds (ETFs) of JPY12 trillion, for Japan real estate investment trusts (J-REITs) of JPY180 billion per year, for commercial papers (CP) by targeting the amount outstanding at about JPY2 trillion, and for corporate bonds by targeting the pre-pandemic level at about JPY3 trillion. The forward guidance has also been maintained, “… the Bank will patiently continue with monetary easing while nimbly responding to developments in economic activity and prices as well as financial conditions. By doing so, it will aim to achieve the price stability target of 2 percent in a sustainable and stable manner, accompanied by wage increases. The Bank will continue with Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control, aiming to achieve the price stability target, as long as it is necessary for maintaining that target in a stable manner. It will continue expanding the monetary base until the year-on-year rate of increase in the observed consumer price index (CPI, all items less fresh food) exceeds 2 percent and stays above the target in a stable manner. The Bank will continue to maintain the stability of financing, mainly of firms, and financial markets, and will not hesitate to take additional easing measures if necessary.” In the Outlook for Economic Activity and Prices that was released on the same day, the BoJ had lowered its FY2024 price outlook from 2.8% to 2.4% due to lower crude oil prices, while revised up FY2025 price outlook marginally from 1.7% to 1.8% from stronger economic activity (than BoJ’s estimate of Japan’s potential growth of around 0.5% to 1.0%), inflation expectations and wage growth. For the real GDP growth outlook, the BoJ revised down its FY2023 outlook from 2.0% to 1.8% to reflect the actual data on business fixed investment has been less than expected. However, the BoJ revised up its FY2024 GDP growth outlook from 1.0% to 1.2% from stronger private consumption and private investments, while the FY2025 GDP growth was left unchanged at 1.0%.

Image

There are a few supporting arguments as to why Japan should be a bright spot in the global equity landscape in 2024. First of all, there is a clear progress towards the reform of corporate governance, encouraging better use of capital, better use of cash, unwinding of strategic shareholdings, investing in growth, review of business portfolios, and increasing shareholder returns. If this is done right, there is high potential for Japanese equity market valuation to further increase, as the return-on-equity ratio (ROE) in comparison to the cost-of-equity ratio (COE) is worse than other developed market counterparts, namely the US and Europe; while the proportion of companies with net cash position is much higher than in the US and Europe. Secondly, there is a substantial scope for improvement in the Japanese consumers’ balance sheet that had been accumulated during the Covid-19 pandemic. There are estimates that this number of consumer savings amounted to around JPY50 trillion. BoJ had mentioned Japanese consumers’ pent-up demand as a positive support for the economy. And while this might lessen in the future, there is a scope for a virtuous cycle from sustainable prices to wage hikes and income, which will flow towards higher spending, and hence, a stronger economy. Thirdly, there is a growing importance of Japanese companies within the global supply chain due to increasing US and China competition. Ongoing support from the Japanese government, as well as the US support for other economies that are non-China, will ensure that the tailwinds for the Japanese semiconductor industry continue.

Image

However, investors looking to allocate to Japan should be aware of some concerns that are brewing. First of all, overweight positioning in Japan has become a common trade, suggesting additional gains are becoming limited. Secondly, if the Fed turns to be more aggressive on rate cuts or the BoJ turns out to be more hawkish on its policy, this outturn could lead to the strengthening of the Japanese yen, which could lead to weakness of Japanese stock share prices (due to translation effect of overseas revenue negatively affecting net profits, as well as yen strength affecting export and tourism competitiveness on the macro level). That being said, we think that Japan remains a bright spot in the global economy this year amid the relatively weaker outlook from other big economies such as Europe and China. Investors looking to allocate to Japanese equities can check out our Principal Japanese Equity Fund A (PRINCIPAL JEQ-A).

Image

Disclaimer: Investors should understand product characteristics (mutual funds), conditions of return and risk before making an investment decision / Master fund has highly concentrated investment in Japan. So, investors have to diversify investment for their portfolios. / Investing in Investment Units is not a deposit and there is a risk of investment, Investors may receive more or less return investment than the initial investment. Therefore, investors should invest in this fund when seeing that investing in this fund suitable for investment objectives of investors and investors accept the risk that may arise from the investment / The fund and/or the master fund may invest in derivatives for hedging purpose depends on Fund Manager decision, investors may receive gains or losses from the foreign exchange or may receive the money less than the initial investment. Past performance does not guarantee future results.