Beyond the Headlines: A Deep Dive into Vietnam’s Stock Market Boom

Image

Vietnam’s economy presents a compelling case for investment, bolstered by several key strengths. First, it boasts a young and abundant workforce, with a median age of just 33 and a working-age population exceeding half of the total population of 99 million. Vietnam offers a competitive workforce with attractive minimum wages compared to regional neighbors. Secondly, its strategic location next to China grants access to cost-effective transportation and well-developed ports. Vietnam’s extensive coastline of over 3,444km is served by 32 shipping routes, including 25 international routes. This maritime strength is further amplified by its 44 major seaports with a combined annual capacity of 500 million tons, along with numerous smaller ports bringing the total to 320. Finally, Vietnam enjoys extensive trade access through its 19 active and planned Free Trade Agreements, the highest number of FTAs by any Southeast Asian countries. Economic forecasts further solidify Vietnam’s attractiveness, projecting it to be the fastest-growing economy in Asia over the next five year. These positive factors also make Vietnam a popular strategic destination to be considered for businesses’ China Plus One strategy.

“What is the China Plus One strategy?”, a reader who’s new to the terminology may ask. China Plus One is a business strategy adopted by companies to diversify their manufacturing and sourcing activities away from sole reliance on China. The ongoing trade war between the US and China has led to increased tariffs and uncertainty for businesses with both direct and indirect business relationship with China. The Covid-19 pandemic had also highlighted the vulnerability of global supply chains that are overly reliant on a single country for the sourcing of manufacturing parts and any raw materials used in the production process. By diversifying the supply chains, companies can lessen the impact of disruptions that might occur in China, such as trade tensions, labor shortages, or natural disasters. Furthermore, China’s labor costs have been rising in recent years, while some developing countries offer even lower production costs. Also, setting up business operations in a new and growing region like Vietnam can help companies gain better access to local markets and benefit from regional trade agreements of that country.

Vietnam’s stock market presents a compelling investment opportunity due to the country’s robust and accelerating economic growth. Several factors underpin this growth trajectory, making Vietnam Asia’s fastest growing economy. Firstly, the Vietnamese government’s significant investment in infrastructure projects like roads, bridges, and airports is enhancing connectivity and attracting foreign investment. Secondly, a burgeoning middle class is driving domestic consumption as people spend more on goods and services. Vietnam’s export sector, a major contributor to the economy, is also poised for a rebound in 2024 as the global economy strengthens. Beyond traditional growth factors, Vietnam is experiencing a tourism boom. Tourist interest is surging, with Google searches for Vietnamese tourism exploding by over 75% in 2023, surpassing regional competitors like Thailand, Indonesia, and the Philippines. This translates to robust international arrivals, with the first two months of 2024 already exceeding 3 million visitors, a significant year-over-year increase.

Foreign direct investment (FDI) is another pillar of Vietnam’s economic strength. FDI registration breakdown showed that foreign capital inflows have been investing heavily into the manufacturing sector. Since the US-China trade war in 2017, we have seen North Asian countries like China, Japan, South Korea, Taiwan, and Singapore allocating more FDIs to Vietnam. The country’s low labor costs and the underlying political stability, despite the recent volatile headlines, make it an attractive destination for FDI, which fuels further investment and growth. Finally, the Vietnamese government’s commitment to science and technology fosters innovation in areas like artificial intelligence and e-commerce, creating exciting new business opportunities. Taken together, Vietnam’s economic dynamism presents a fertile ground for investors looking to capitalize on a rapidly growing and multifaceted market.

Vietnam’s emergence as a manufacturing powerhouse presents a compelling investment opportunity. A structural shift is underway, with manufacturers relocating to Vietnam to capitalize on its advantages. This trend is evident in Vietnam’s impressive growth in both Foreign Direct Investment (FDI) and exports to the US, compared to maturing China. While China’s total export volume remains larger, Vietnam’s exports to the US have been surging at an average of 15% annually since 2008 – a rate more than three times faster than China’s 4.6% growth rate. This robust export performance translates to FDI inflows growing at an average of 4.7% per year in Vietnam, compared to China’s stagnant FDI. Vietnam’s export success story is further reflected in this rapidly growing share of global exports over the past two decades, mirroring India’s similar rise. Recognizing this potential, the Vietnamese government is actively fostering the manufacturing sector, aiming to increase its contribution to GDP from 25% to 30% by 2030. This strategic focus on manufacturing positions Vietnam as a prime destination for investment, offering access to thriving production hub with strong growth prospects.

Vietnam is rapidly establishing itself as the new tech hub of Asia, attracting significant investments and production facilities from leading global companies. This surge in tech prominence is fueled by Vietnam’s cost competitiveness, which has surpassed established players like Korea and Taiwan in terms of export value. The trend of supply chain relocation towards Vietnam is undeniable. Take Apple’s supplier base for instance: Vietnam has witnessed the highest growth in Asia when comparing the number of official Apple suppliers in 2022 to 2016. This growth is indicative of a broader movement by tech giants to leverage Vietnam’s advantages. Beyond Apple, renowned companies like Intel, Samsung, Amkor, Hyundai Motor, and LG have chosen Vietnam as their new production base. The tech ecosystem is further bolstered by the presence of Qualcomm’s R&D center, with NVIDIA also planning to establish one in Vietnam. The Vietnamese government is actively fostering this growth by preparing a diversified tax scheme across different industry qualifications. Expected to be implemented in 2024, these tax incentives will further entice businesses to set up shop in Vietnam, lowering their effective tax rates and propelling the country’s tech sector to even greater heights. This burgeoning tech landscape in Vietnam presents a lucrative investment opportunity for those seeking exposure to a dynamic and fast-growing market.

Vietnam stands out as a compelling investment opportunity within ASEAN thanks to its exceptional cost competitiveness and strong trade relationships. Compared to its regional peers, Vietnam boasts significant advantages in terms of labor costs, rent, construction expenses, and even electricity prices. Furthermore, Vietnam’s workforce is demonstrably high-quality. Vietnamese students consistently rank highly in international assessments like PISA test. Stands for the Programme for International Student Assessment, PISA test is a worldwide study by the Organisation for Economic Co-operation and Development (OECD) in member and non-member nations that measures 15-year-old students’ problem-solving ability and cognition. In the PISA 2022 test, Vietnamese students placed 34th globally and in second place in ASEAN behind only Singapore in mathematics, science, and reading proficiency.

Beyond its competitive workforce, Vietnam enjoys extensive trade access through its 19 active and planned Free Trade Agreements (FTAs). As mentioned in the beginning, this is the highest number in Southeast Asia. These agreements encompass a remarkable 60 countries, translating to over 60% of global GDP being accessible through trade deals with Vietnam. Additionally, Vietnam’s commitment to international partnerships is further underscored by its recent upgrade to a Comprehensive Strategic Partnership (CSP) with the US in September 2023. This elevated status signifies the strongest possible diplomatic relationship for Vietnam and is expected to yield significant benefits. Increased technology transfer and advancements in Vietnam’s digital infrastructure and semiconductor industry are expected. Moreover, the CSP fosters a more stable and secure environment for foreign investors, potentially leading to a surge in FDI that will create jobs and propel economic growth. A deeper trade relationship with the US could also emerge from this partnership, potentially involving tariff reductions, new trade agreements, and expanded market access for Vietnamese goods and services.

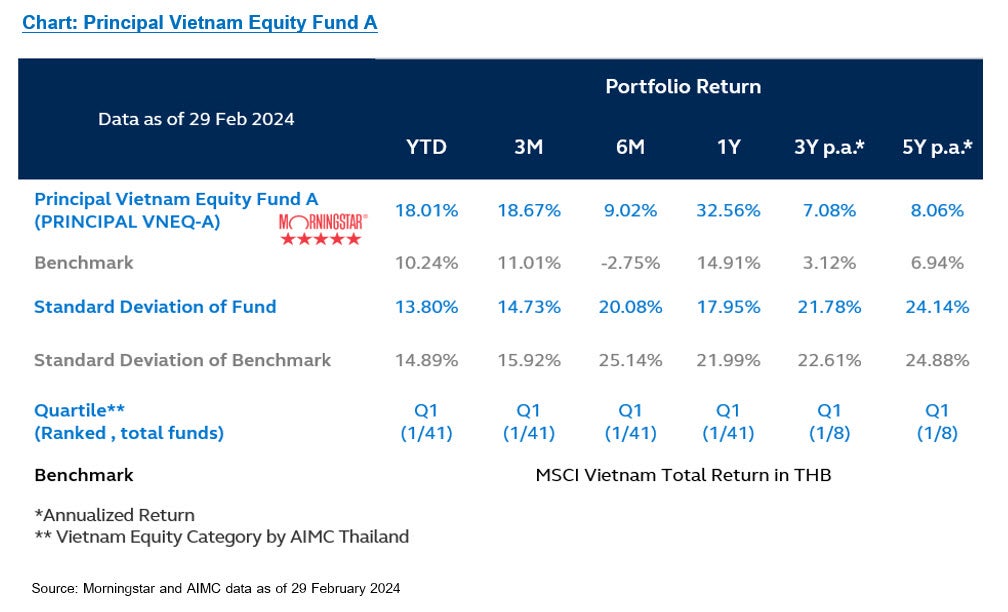

Vietnam’s stock market has emerged as a star performer in ASEAN, offering investors a compelling opportunity. While the MSCI Vietnam Index delivered a return of 5.0% in 2023 when translated to Thai baht, our Vietnam’s very own fund – Principal Vietnam Equity Fund (PRINCIPAL VNEQ) – had outdone the market quite handsomely, achieving an impressive 11.9% return and ranking as number one among 41 Vietnam equity funds that were registered in Thailand according to data from Morningstar. Furthermore, according to Morningstar, the median return (50th percentile rank) of the Vietnam Equity fund category in Thailand was only 6.6% in 2023. Beyond the headline performance mentioned, Vietnam’s stock market boasts surprising liquidity. Trading volumes have improved significantly over the past year, with daily liquidity already on par with established markets like Indonesia and Singapore. Furthermore, when measured as a percentage of market capitalization, Vietnam’s daily liquidity now leads the pack among Indonesia, Malaysia, Philippines, Singapore, and Thailand.

The robust market environment coincides with exceptional corporate earnings growth. At 32% in 2024 and 28% in 2025, Vietnam boasts the highest earnings per share growth in ASEAN, doubling the rate of its regional neighbors Thailand, Indonesia, Philippines, and Malaysia. While these high earnings are impressive on their own, Vietnam’s valuation makes them even more attractive. The market currently trades at a PE ratio of just 11 times 2024 earnings, significantly lower than the 14-15 range typical of other countries in the region. This combination of high earnings growth and a low valuation creates an exceptional opportunity, especially considering that earnings growth in other regional markets is only half that of Vietnam. Vietnam thus offers a confluence of strong performance, improving liquidity, exceptional corporate earnings growth, and attractive valuations. These factors combine to make Vietnam a compelling investment destination within ASEAN, especially for investors seeking exposure to a dynamic and rapidly growing market.

Vietnam’s stock market is on the cusp of a significant transformation, with a clear path towards an upgrade from Frontier Market to Emerging Market status. This presents a compelling investment opportunity for those seeking exposure to a high-growth market on the verge of a major revaluation. Two key hurdles currently stand in the way of the upgrade: the pre-trade deposit requirement for foreign investors and limitations on foreign ownership. However, the Vietnamese government is actively addressing these challenges. The pre-trade deposit requirement is expected to be eliminated by late 2024 or within 2025, while foreign ownership limit problem is expected to be addressed through increased quotas and the launch of depositary receipts (NVDRs) sometime later in 2025. Given the timeline for these improvements, it’s expected that FTSE will likely move forward with the upgrade before MSCI. This is because FTSE only requires one of the two criteria – the removal of the pre-trade deposit requirement – to be met for the upgrade, whereas MSCI requires both to be met.

Historical data on similar market upgrades is highly encouraging. Studies show that PE ratios typically experience a 35% rerating within two years of the upgrade proposal. This suggests significant potential for valuation growth in the Vietnamese stock market. Furthermore, past examples like Thailand’s introduction of NVDRs in 2001 provide concrete evidence of the positive impact of such reforms. Following the introduction of NVDRs, Thailand witnessed a 50% surge in foreign inflows over the next five years. Vietnam’s planned implementation of NVDRs is likely to have a similar effect, attracting a wider pool of foreign investors and boosting overall market liquidity. By investing in Vietnam’s stock market now, investors can potentially benefit from a confluence of factors: a fast-growing economy, improving market accessibility, and the potential for significant PE ratio expansion upon achieving Emerging Market status. This combination creates a compelling entry point for investors seeking exposure to a dynamic and rapidly evolving market on the cusp of transformation.

Image

Image

Image

Disclaimer: Investors should understand product characteristics (mutual funds), conditions of return and risk before making an investment decision / PRINCIPAL VNEQ has highly concentrated investment in Vietnam, so investors have to diversify investment for their portfolios. / Investing in Investment Units is not a deposit and there is a risk of investment, Investors may receive more or less return investment than the initial investment. Therefore, investors should invest in this fund when seeing that investing in this fund suitable for investment objectives of investors and investors accept the risk that may arise from the investment. / The fund and/or the master fund may invest in derivatives for hedging purpose depends on Fund Manager decision, investors may receive gains or losses from the foreign exchange or may receive the money less than the initial investment. / Copyright @ 2024 Morningstar Thailand All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance does not guarantee future results.