CIO View: August 2025

Image

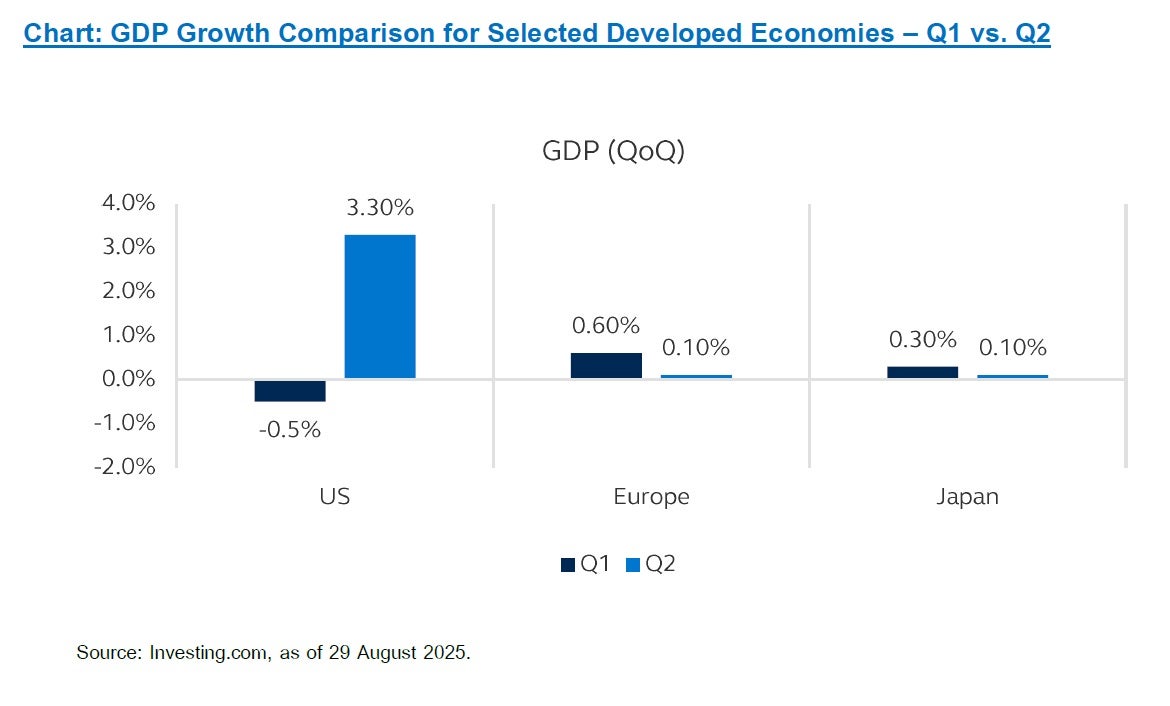

The US economy grew at an annual rate of 3.3% in the second quarter 2025, rebounding from a 0.5% contraction in the first quarter, beating consensus of a 3% rise. The largest contributor to the Q2 GDP growth was a sharp decline in imports. In the first quarter, the surging in imports took a toll on economic growth, but that trend reversed in the second quarter as businesses drew from their existing inventories instead of importing. Consumer spending, which accounted for 70% of the US economy, picked up sharply in the second quarter to a 1.4% rate, up from the 0.5% growth in the first quarter. But, combined with the previous data, it marks the two slowest quarters of spending since the pandemic. Meanwhile, businesses slowed their spending sharply during the same period, to 1.9% from 10.3%, mostly reflecting a recalibration from the front-loading of spending that happened earlier in the year. However, the employment growth was weaker than expected in July, while the nonfarm payrolls count for the prior two months was revised down by a massive 258,000 jobs. Recent signs of a cooling labor market have intensified debates around the health of the U.S. economy and the path of monetary policy. July’s weaker-than-expected jobs report elevated concerns and added to market volatility already heightened by tariff announcements. The odds of a September rate cut spiked, alongside uncertainty about whether the Fed is already behind the curve.

The Eurozone economy grew 0.1% quarter-on-quarter in the second quarter of 2025, its weakest performance since the fourth quarter in 2023, slowing from 0.6% in the previous quarter. The slowdown follows a Q1 boost from tariff front-loading, while lingering uncertainty over US trade measures has prompted greater caution among businesses and households. Among the bloc’s economies, GDP contracted in German (-0.1% vs +0.3%), Italy (-0.1% vs +0.3%), and Ireland (-1% vs +7.4%), while GDP accelerated in France (+0.3% vs +0.1%) and Spain (+0.7% vs +0.6%). In contrast, Japan’s economy showed stronger-than-expected growth in the second quarter as export volumes held up well against new U.S. tariffs. Japan’s GDP grew by 0.3% quarter-on-quarter compared to a 0.1% growth seen in the first quarter, exceeding the median market forecast of a 0.1% increase. Private consumption, which account for more than half of Japan’s economic output, rose 0.2%. It grew at the same pace as the previous quarter. Capital spending, a key driver of domestic demand, rose 1.3% in the second quarter. Net external demand contributed 0.3% to growth, versus a 0.8% negative contribution in the January-March period. The stronger-than-expected GDP provides the Bank of Japan (BOJ) with more leeway to consider resuming interest rate hikes later in the year.

Image

In monetary policy development, Federal Reserve Chair Jerome Powell delivered his annual address at the central bank’s annual symposium in Jackson Hole on 22 August 2025. His speech was widely interpreted as a signal that the Fed is moving closer to a rate cut. He acknowledged a "challenging situation" where risks to employment are on the downside while inflation risks are tilted to the upside. However, he stated that the "shifting balance of risks may warrant adjusting our policy stance." This dovish tone led to an increase in market expectations for a rate cut at the next Federal Open Market Committee (FOMC) meeting in September. A key factor supporting the case for a rate cut is the softening of the U.S. labor market. Powell noted that job growth has slowed substantially, and while the unemployment rate remains historically low, other indicators suggest that "downside risks to employment are rising." He highlighted the "curious kind of balance" in the labor market, where both the supply of and demand for workers are slowing. Powell addressed the new challenge posed by higher tariffs, which he said have "begun to push up prices in some categories of goods." While he acknowledged that the effects of tariffs on consumer prices are now "clearly visible," he expressed a "reasonable base case" that the effects will be "relatively short lived—a one-time shift in the price level." This suggests that the Fed does not see tariffs as a source of ongoing, long-term inflation that would require further tightening of monetary policy.

In a speech on 20 August 2025 at the International Business Council of the World Economic Forum, The European Central Bank (ECB) President Christine Lagarde addressed the tenuous resilience of the global economy. She noted that while the euro area economy has been resilient, this was partly due to a temporary surge in exports from businesses front-loading their purchases ahead of new U.S. tariffs. Looking ahead, according to the Eurosystem’s June projections, growth is expected to slow in the third quarter as the front-loading spending unwinds. The ECB has adopted a wait-and-see approach, with policymakers emphasizing the need to assess the full impact of ongoing trade disputes and other geopolitical risks. The ECB’s staff will factor the implications of a new EU-US trade deal, which imposes higher tariffs on some Euro area goods, into its upcoming September projections. The Bank of Japan’s (BOJ) “Summary of Opinions” from its July 2025 meeting showed that the BOJ needed at least two to three more months to assess the impact of US tariff. One member suggested that it may be possible for the BOJ to exit from its current wait-and-see stance, perhaps as early as the end of this year, if the impact of US tariff on Japan’s economy remains minimal. On 1 August 2025, the People’s Bank of China (PBOC) held its semi-annual work conference to review its performance in the first half of the year and outline its policy priorities for the second half. The PBOC reiterated its commitment to a moderately loose monetary policy. The central bank stated it would increase the intensity and forward-looking, targeted, and effective nature of its policy adjustments. Thus suggests a continued willingness to use a variety of tools, including structural instruments, to support the real economy. In addition, the PBOC would double down on efforts to manage financial risks and support the stability of the capital and real estate markets. On 20 August 2025, The PBOC kept the 1-year loan prime rate unchanged at 3.0% and kept the 5-year loan prime rate unchanged at 3.5%. The decision was in line with market expectations.

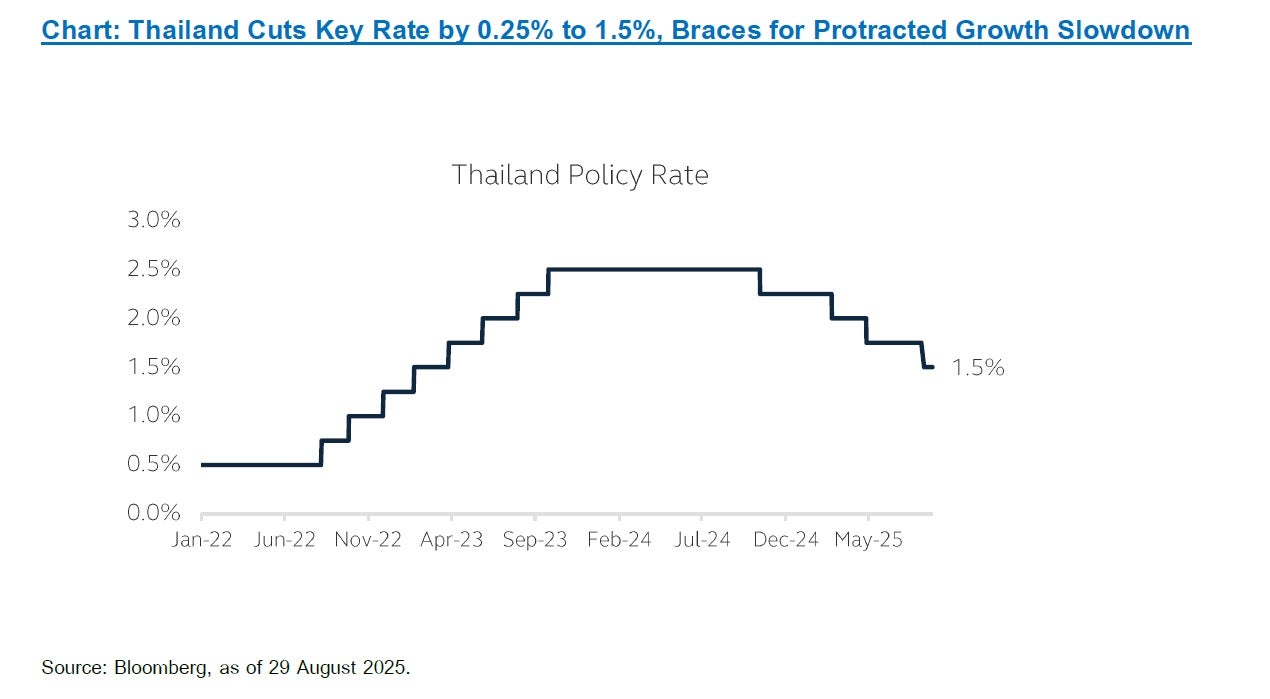

The Bank of Thailand’s (BOT) Monetary Policy Committee (MPC) voted unanimously on 13 August 2025 to lower the rate by 25 basis points to 1.50%, as it looks to support a sluggish economy grappling with negative inflation and the impact of US tariffs. In the current easing cycle, the central bank has lowered the policy rate four times by 100 basis points starting in October last year, followed by rate cuts in February, April, and August this year, each time by 25 basis points. MPC secretary Sakkapop Panyanukul said the committee wants monetary policy to be more accommodative to ensure financial conditions remain conducive to business adjustments, easing the burden on vulnerable groups such as small and medium enterprises (SMEs) and low-income households. Headline inflation has been in negative territory since April and has consistently undershot the central bank’s 1-3% target range throughout this year. The committee also acknowledged that more signs of weakness in the economy are emerging. The central bank forecasts GDP growth of 2.3% this year and will review projections for both 2025 and 2026 at the next MPC meeting in October.

Image

On 15 August 2025, the Thai House of Representatives approved the government's budget bill for the 2026 fiscal year. The Bt3.78 trillion bill was passed with 257 votes in favor and 230 against. The budget bill will now be sent to the Senate for consideration. According to the Thai parliamentary procedure, the Senate has 20 days to review the bill. After that, it requires royal endorsement to become enacted into law, with the new fiscal year set to begin on 1 October 2025. The budget aims to increase government spending to stimulate the economy, which has been facing challenges from high household debt and international trade issues. The budget is intended to support various government policies and national strategic plans, with a focus on areas like infrastructure development and enhancing human capital.

The Constitutional Court has summoned suspended Prime Minister Paetongtarn Shinawatra to testify as part of the hearing. She appeared before the court on 21 August 2025 to provide her prepared testimony. The court is also hearing from other witnesses, including the Secretary-General of the National Security Council and individuals who filed complaints. The next steps involve the closing statement, which the Court has fast-tracked to be delivered on 25 August 2025, ahead of the original schedule of 27 August 2025. This is to allow the judges more time to consider the case before the final verdict on 29 August 2025. If Paetongtarn is found guilty in this case, the Prime Minister’s position will be up for change, which could lead to a shift in leadership, whether from Pheu Thai or another coalition party. The chance of a snap election would increase, opening the door for a new political administration.

In today’s unpredictable market environment, investors are often faced with sharp swings, conflicting headlines, and a constant stream of noise that can make decision-making feel overwhelming. Volatility isn’t just a headline—it’s a reality that affects portfolios, emotions, and long-term goals. That’s where multi-asset investing comes in. By combining different asset classes—such as equities, bonds, real estate, and alternatives—investors can build portfolios that are more resilient, better diversified, and designed to weather market turbulence. Mult-asset strategies can help investors stay steady, stay invested, and stay focused on what truly matters: long-term growth of your portfolios. Diversification across asset classes, geographies, and sectors remains the cornerstone of resilient portfolio construction. Our recommendation to focus on asset allocation diversification is increasingly relevant in today’s world that is faced with continuous uncertainties. Multi-asset funds such as Principal Multi Asset Balanced Fund (PRINCIPAL MABALANCED) is appropriate to recommend to clients to stay invested in markets with a balanced exposure to asset classes. Principal Multi Asset Income Fund (PRINCIPAL MAINCOME) is our recommendation to more conservative clients who prefer to have higher exposure to less volatile asset than risky asset classes. Principal Multi Asset Global Fund (PRINCIPAL MAGLOBAL) would be more suitable to the more aggressive clients, who are more comfortable to have majority of the portfolio invested in more volatile risky assets to generate growth for the long term. We believe that under the current environment, flexibility matters now more than ever due to the elevated geopolitical risk, tariff-driven cost pressure to businesses, as well as diverging central bank policies. Investors should stay diversified and agile to weather potential shocks and to be able to seize opportunities when they emerge. The multi asset funds can act as a core portfolio, providing stability and adaptability in uncertain economic conditions. Investors can complement their core holdings with a global fixed income fund to add a conservative tilt to the portfolio; or complement it with a thematic growth fund for a growth tilt to the portfolio. For example, investors can choose to invest in the Principal Multi Asset Balanced Fund (PRINCIPAL MABALANCED), which offers a balanced allocation between equities and fixed income, helping to mitigate volatility while seeking steady returns as a default portfolio, and then add to their portfolio with other focused strategies of their choice to make it more personalized.

I would like to close this month’s CIO View with a recommendation to read a very interesting investment article written by one of our U.S. colleagues from the Global Insights team. As investors continue to weigh global diversification against the enduring strength of U.S. markets, it’s worth revisiting the foundational role U.S. equities play in long-term portfolios. One recent perspective that captures this well comes from Principal Asset Management, where Mike Reidy outlines why U.S. equities remain a cornerstone of retirement investing. In his 31 July 2025 article titled “Still exceptional: Why U.S. equity remains a cornerstone of retirement portfolios”, our U.S. colleague Mike Reidy explores why U.S. equities continue to play a vital role in long-term retirement strategies, even as investors increasingly look abroad. While international markets have gained attention due to favorable valuations and currency dynamics, Reidy argues that the U.S. market’s structural strengths—such as deep capital markets, robust legal frameworks, and a dynamic innovation ecosystem—remain unmatched. He also highlights the historical resilience of U.S. equities, which have consistently outperformed through periods of uncertainty. For investors focused on long-term wealth creation, maintaining a core allocation to U.S. equities remains a prudent choice. Read the full article at https://www.principalam.com/us/insights/asset-allocation/still-exceptional-why-us-equity-remains-cornerstone-retirement-portfolios.

Recommended Funds

Fund Recommend | Fund Information |

| Principal Multi Asset Income Fund A (PRINCIPAL MAINCOME-A) | https://www.principal.th/en/principal/MAINCOME-A |

| Principal Multi Asset Balanced Fund D (PRINCIPAL MABALANCED-D) | https://www.principal.th/en/principal/MAGLOBAL-A |

| Principal Multi Asset Global Fund A (PRINCIPAL MAGLOBAL-A) | https://www.principal.th/en/principal/MAGLOBAL-A |

Disclaimer: Investors should understand product characteristics (mutual funds), conditions of return and risk before making an investment decision./ PRINCIPAL MAGLOBAL has Master fund has highly concentrated investment in United States, So, investors have to diversify investment for their portfolios. / Investing in Investment Units is not a deposit and there is a risk of investment, Investors may receive more or less return investment than the initial investment. Therefore, investors should invest in this fund when seeing that investing in this fund suitable for investment objectives of investors and investors accept the risk that may arise from the investment./ Investors may lose or receive foreign exchange gains or receive a lower return than the initial investment. / The fund and/or the master fund may invest in derivatives for hedging purpose depends on Fund Manager decision, investors may receive gains or losses from the foreign exchange or may receive the money less than the initial investment. / Past performance does not guarantee future results.