CIO’s View July 2022 Encouraging Sign for Asia

CIO’s View July 2022 Encouraging Sign for Asia

By Supakorn Tulyathan, CFA, Chief Investment Officer

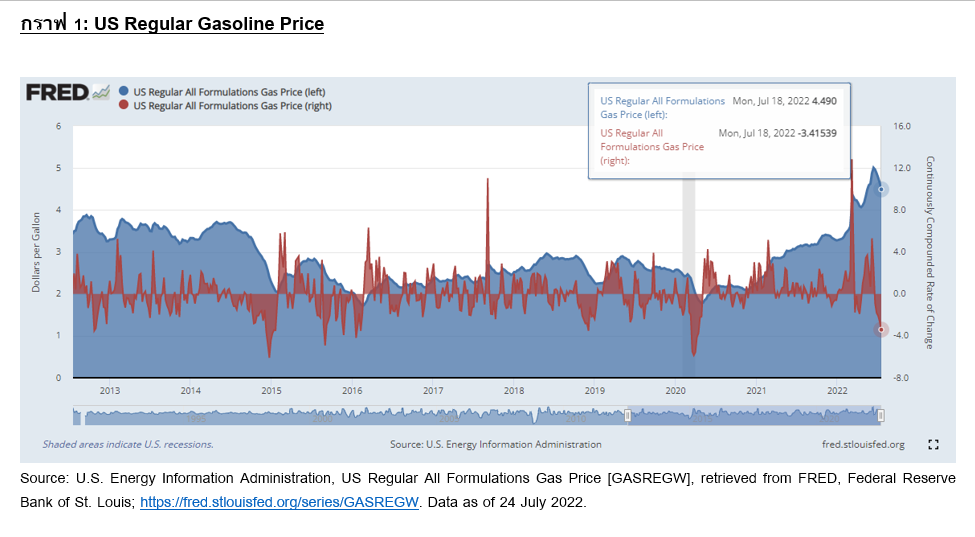

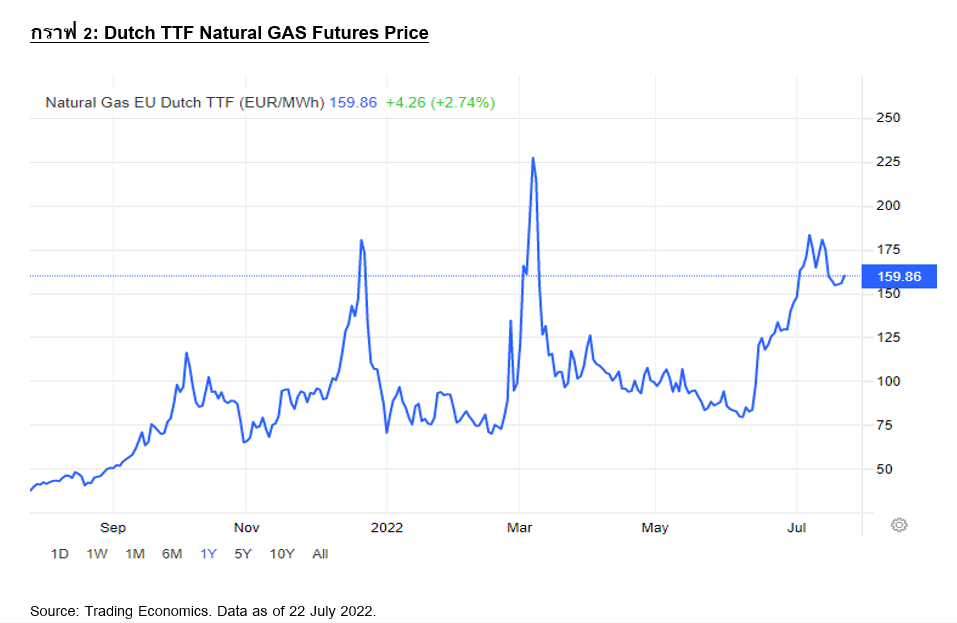

This month’s observation of PMI data has seen a significant loss of momentum in the US and Europe. The US has seen its Manufacturing PMI data in July declined to 52.3 from 52.7 in June; while the Services PMI data in July collapsed to 47.0 from 52.7 in June. In Europe, the Eurozone Manufacturing PMI in July had fallen to 49.6 from 51.0 in June; while the Services PMI had fallen to 50.6 from 53.0 in June. These data releases point to DM economies that are losing momentum in their economic activities, which should lead to less upside pressure in the inflation data in the future. However, US inflation data has not shown a declined that everyone has been waiting for, as US CPI inflation continued to make new high at 9.1% y/y in June. US core inflation, on the other hand, has declined from the high of 6.5% in March to 5.9% in June. Europe will be reporting its July CPI inflation later in the month; however, June number was 8.6%, up from 8.1% in May. Core inflation in June was 3.7% from 3.8% in May. In both DM regions, the energy component of CPI has shown alarming increase, with the latest June numbers being 41.6% y/y in the US, and 42% y/y in Europe. We have seen a bit of good news on declining gasoline prices in the US, with the latest US Regular All Formulations Gas Price (chart’s shown below) declining to $4.49 per gallon, representing the fifth week of negative growth, and possible relief in US inflation over the next three months. Meanwhile, EU natural gas price (chart’s shown below) remained high near €160 per megawatt hour, suggesting elevated Europe’s inflation over the next three months

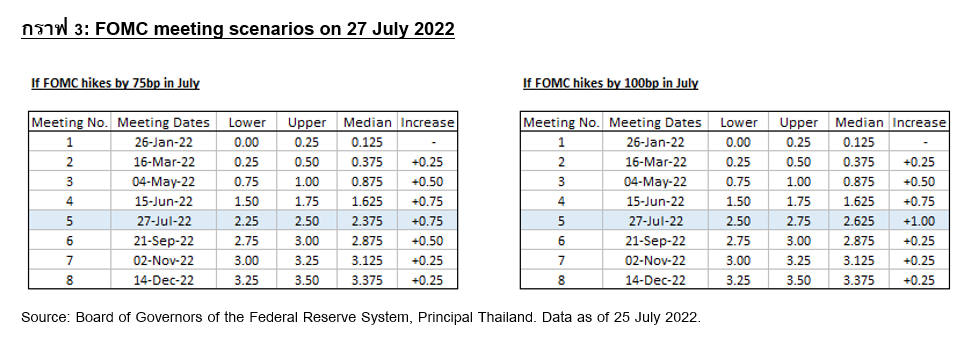

Looking back at the FOMC meeting in June, the Fed had upgraded its end-2022 Fed funds rate to 3.4%, while maintaining the longer run (aka. neutral rate) at 2.5%. If this week’s FOMC on July 27 happens exactly as the consensus expects, we will be seeing the Fed raising the Fed funds rate by 75 basis points, taking it to 2.5%, which is exactly where the neutral rate is, according to the FOMC’s dot plot (Fed’s own forecasts). However, as the surprise ECB monetary policy meeting had shown (which we will talk about next), there is always a chance that the Fed might go for a larger move, especially as the inflation numbers continue to surprise higher. So, if the Fed decides to move by 100 basis points this time, the Fed funds rate will start to be in restrictive territory beginning this week (chart’s shown below). July meeting is important because after the Fed funds is at or a little higher than neutral rate this week, the Fed will probably start to move in smaller steps for the rest of the year, by 25 basis points at each of the remaining three meetings if their 3.5% at end-2022 is still valid.

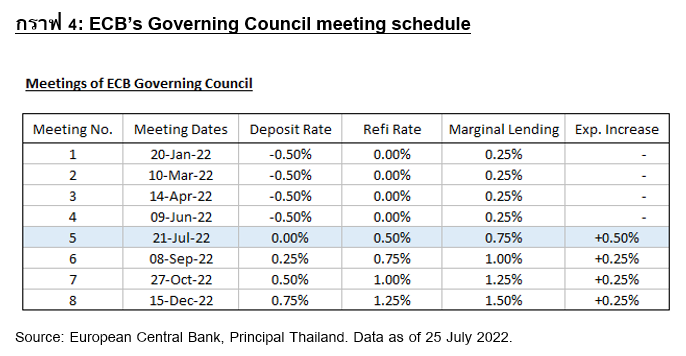

The ECB has raised its policy rates on July 21 by more than the market had expected. The deposit rate, refinance rate, and marginal lending facility rate have all been announced to increase by 50 basis points for all three policy rates (chart’s shown below), which will be effective from July 27 onwards, and will have taken the Eurozone out of the negative interest rate regime that had been in place since 2014. This was against market expectation of just a 25 basis point move. ECB stated that upcoming meetings will become more data dependent. Right now we see 25 basis point move at each of the remaining three meetings, given upside risks to inflation, but downside risk to growth. The ECB announced that they intends to continue reinvesting, in full, the principal payments from maturing securities purchased under the Asset Purchase Program (aka. APP) for an extended period of time, and for as long as necessary to maintain ample liquidity. As for the Pandemic Emergency Purchase Program (aka. PEPP), they intend to reinvest the principal payments from maturing bonds until at least the end of 2024. The ECB also launched a new Transmission Protection Instrument (aka. TPI), which is an anti-fragmentation tool aimed at supporting effective transmission of monetary policy. The TPI will have no pre-defined restrictions on bond purchases or its lifespan, making it a permanent addition to the ECB’s monetary tools. On the political front, Italy’s President Sergio Mattarella had dissolved parliament last week, triggering a snap election following the resignation of the country’s Prime Minister Mario Draghi; while the election date have been scheduled for September 25. Given the rising political risk in Italy, the additional TPI by the ECB will be useful for managing any undesirable effect on Italy’s bond yield.

As widely expected in Japan, the BOJ maintained its -0.1% target for short-term rates and that of 10-year bond yields around 0% on July 20. In their updated quarterly economic projections, the board raised its core consumer inflation forecast to 2.3% from 1.9% previously for the current fiscal year ending March 2023. It also raised its forecast for 2024 to 1.4% from 1.1%. However, the growth forecast for this fiscal year has been cut to 2.4% from 2.9% due to downside risk to growth from supply constraints, rising commodity prices and the pandemic. Despite criticisms of the current policy, Governor Kuroda pushed back against adjusting the Yield Curve Control (aka. YCC) in response to the sharp yen depreciation or the breaching of the upper band of the 10-year yield target. He believes the monetary policy tightening needed to stem the drop in the yen would be too drastic and imperil growth.

Things are turning brighter for the exporters in Asia. Supply constraints resulting from the zero-Covid lockdown policy in various cities in China have eased, and Chinese import demand have rebounded. Taiwan exports rebounded to 15.2% in June from 12.5% in May; while export orders rebounded to 9.5% in June from 6.0% in May (and -5.5% in April). Japan’s exports also rebounded to 19.4% in June from 15.8% in May, led by a rebound of exports to China. The encouraging sign for China and its positive spillover to Asia led us to become positive on Chinese equity funds and Asian equity funds in the past couple of months. We recommend Principal China Equity Fund A (PRINCIPAL CHEQ-A), Principal China Technology Fund A (PRINCIPAL CHTECH-A), and Principal Asia Pacific Dynamic Income Equity Fund A (PRINCIPAL APDI-A) for China and Asia investments. The recent issue of mortgage suspension requests is putting a near-term limit on China’s recovery. The total value of affected mortgages is estimated at around CNY130 billion, which is translated to around 2.1% of mortgage loans outstanding. At this point, we believe that China’s policymakers should be able to contain any negative spillovers. Although, this would tend to put a limit on growth rebound via house prices, ability of banks to increase loans, household wealth and consumption. We would carefully monitor the development on this issue at this point, but would view any correction in the Chinese equity market as an entry point to accumulate.

Recommended Funds

Principal China Technology Fund (PRINCIPAL CHEQ) : https://www.principal.th/en/principal/CHEQ-A

Principal China Technology Fund (PRINCIPAL CHTECH) : https://www.principal.th/th/principal/CHTECH-A

Principal Asia Pacific Dynamic Income Equity Fund (PRINCIPAL APDI) : https://www.principal.th/en/principal/APDI-A

Download CIO’s View July 2022 Encouraging Sign for Asia, click